Brent Crude and West Texas Intermediate Oil both fell to their lowest levels since January as fresh recession fears swept the market. Brent dropped to $87 a barrel and WTI to $81. The prices dropped following OPEC’s decision to cut the production by 100,000 barrels a day of supply from October.

In recent months with the Russian and Ukraine conflict raging, OPEC had to lift production as supply dipped. However, with the decreasing health of the global economy and a incredibly strong US dollar demand for overseas oil has dipped. Poor economic data from China and its Covid zero strategy has also pushed concerns of weaker demand.

In fact, China’s crude oil important dropped by 9.4% from a year earlier signalling the slowdown in demand. Furthermore, with the US federal reserve expected to remain hawkish until inflation is back to a sustainable level, in the short term there is little resistance in the way of the US dollar continuing to grind its way higher, further pressuring the price of oil. Whilst the current dip may provide some relief for consumers, with uncertainty from the Kremlin and Putin potentially capping their energy exports, the short term volatility will likely continue.

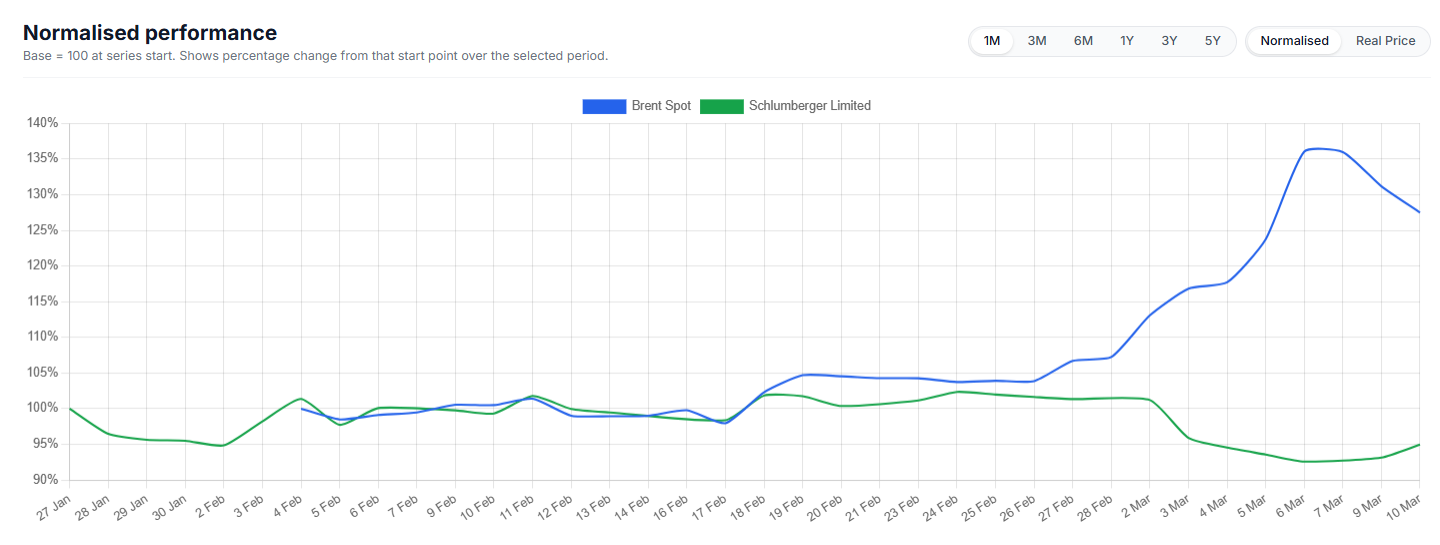

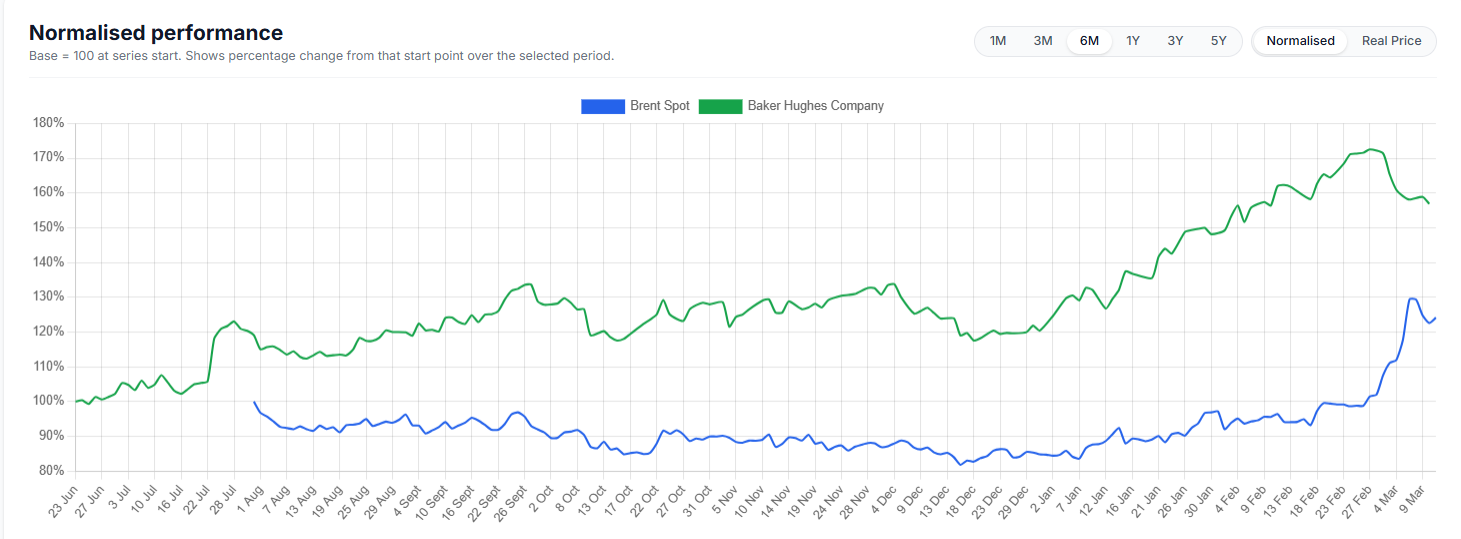

As it can be seen from the charts below, both WTI and Brent have broken down through their key support levels. The price may struggle to fall lower in the immediate short term and may need to consolidate in the short term before pushing lower again.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. 免责声明:文章来自 GO Markets 分析师和参与者,基于他们的独立分析或个人经验。表达的观点、意见或交易风格仅代表作者个人,不代表 GO Markets 立场。建议,(如有),具有“普遍”性,并非基于您的个人目标、财务状况或需求。在根据建议采取行动之前,请考虑该建议(如有)对您的目标、财务状况和需求的适用程度。如果建议与购买特定金融产品有关,您应该在做出任何决定之前了解并考虑该产品的产品披露声明 (PDS) 和金融服务指南 (FSG)。

.jpeg)