We are less than three weeks away from the ASX earning season and we are less than two weeks away from the earnings season in the US. So, we need to start prepping for trades and opportunities now. First and foremost, do not forget that confession season is well and truly upon us here in Australia.

Downgrades clearly have been coming from the discretionary sector; we've even seen companies hit the wall with the likes of Booktopia going into administration. There are some clear thematics that are growing in the Australian market. Energy, while the worst performing sector for the financial year 2024, may actually show you that earnings were slightly above expectation on higher than expected oil prices.

Materials led in the main by BHP, Rio and FMG Have once again benefited from higher than expected iron ore prices. It also benefited from a lower than expected AUD/USD where average FX prices were expected to be between $0.68 and $0.73 but instead have averaged between $0.63 and $0.67. What we're looking for is operational costs, overall margins and forward looking guidance, something that these firms have lacked in the last three financial updates.

Watch very closely for the excitement that will come from things like copper at the expense of the issues that are facing nickel lithium and other transition metals that have had really tough periods in FY24. Moving to the banks this is a sector people argue is fully valued. It's not hard to argue when through the financial year CBA made record all time highs several times and is still within a whisker of its record all time high.

Higher interest rates will indeed improve net interest margins. However, the unknown question and what we need to see at its August full year earnings is the impact higher rates are having on bad and doubtful debts, the possible increase in provisioning and more importantly the impact its having on new loans and refinancing. There is an argument to be made that banking is possibly fully priced and no matter what result is delivered won't necessarily create a leg further higher.

Finally, you can't go past consumer staples and discretionary. Retail sales numbers over the last 18 months have actually shown discretionary spending At or above 2022 levels although month on month figures have been erratic. The question that will come for discretionary spending is margins and how much sales revenue translates to the bottom line in earnings and profit.

Staples on the other hand have seen consistent movement on the revenue line but the question will be the margin and after the very targeted senate inquiry into supermarkets any sign profits are above trend may actually be met with concern as geopolitics raises its head. 33 times in 2024 the US 500 and the Tech 100 have made record highs – can it continue? Look into the US and the ending season that it is about to undertake. We have to look at several core thematics that are likely to be raised.

Artificial Intelligence (AI) The question you’ve got to ask is: is the time frame long or short? We raised this Mag 7 stocks etc Microsoft, Amazon, Alphabet, apple have clear potential. They are evolving their business models and see the integration of AI as the future of their individual businesses.

That will likely come up in their numbers but it will come with operational and initial upfront costs as the integration of AI begins. This is all long term may not fully capture short term opportunities which is still presenting very much in the semiconductor providers. NVIDIA and Advanced Micro Devices are taking full advantage and monetizing the compute cycle.

This clearly won't be forever because it will go from semiconductors to infrastructure to software and therefore the flows will move back towards the bigger end of town but overall the AI thematic still flows towards the semiconductors for now and that's likely to be shown in the earnings season that's coming. Data Centres That brings us to data centres because the potential for ensuring AI requires a heck of a lot of storage and a heck of a lot of processing. There are estimates the data centres will need to grow by 420% in Europe and 250% in the US by 2035 based on the rate of growth in AI right now.

Therefore, we need to watch providers like Dell Technologies and Intel which are big providers of data centres currently. We think the market hasn’t fully appreciated DC needs in the AI revolution. Cybersecurity The final key theme in the AI data centre technology space that we also think needs to be watched is cyber security.

It's been something along the lines of a 70% increase in ransomware attacks over the past 24 months. The regulatory requirements and the budgets required to deal with these increased threats is only just beginning. That brings players like Fortinet to the fore IT programmes and it's pensively to develop programs for enterprise makes it an interesting one going forward.

GLP-1 ‘Weight Loss’ Medicines Another theme of being a really strong driver of the S&P 500 is the rise of GLP-1 medicines. The weight loss craze that has come off the back of this Amazon has been incredible. Initially obviously developed for diabetes but having an additional effect of weight loss has created a product out of nowhere.

Eli Lilly and Co is a key player in this space with its GLP one class medicines already approved by the FDA. It's been launched in the US and its oral intake has posted adoption. It is not the only one in this space but shows very clearly the impact weight loss medicines are having on earnings.

The caveat we have though is side effects and long term impacts are still being found and could be said as a capping issue on price. Whatever way you look at it the US dating season however will be incredibly exciting and it is the reason The US markets continue to see huge capital inflows as they are much more exciting in this current environment than traditional value markets such as Australia.

By

Evan Lucas

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs.

Jika Anda menghabiskan waktu melihat terminal perdagangan, Anda telah melihatnya. Judul berita pecah, garis grafik terputus, dan tiba-tiba semua orang bergegas menuju pintu keluar yang sama atau pintu masuk yang sama. Sepertinya kekacauan. Dalam praktiknya, seringkali merupakan rantai respons mekanis.

Ini penting karena beberapa alasan. Banyak pembaca menganggap cerita itu adalah perdagangan. Itu tidak. Ceritanya, apakah itu keputusan suku bunga, kejutan pasokan atau kehilangan pendapatan, adalah bahan bakar dan pedoman adalah mesinnya.

Di bawah ini adalah tujuh strategi inti yang sering digunakan dalam perdagangan kontrak untuk perbedaan (CFD). Dengan CFD, Anda tidak membeli aset yang mendasarinya. Anda berspekulasi tentang perubahan nilai. Itu berarti seorang pedagang dapat mengambil posisi panjang jika harga naik, atau posisi pendek jika turun.

Tujuh strategi yang harus dipahami terlebih dahulu

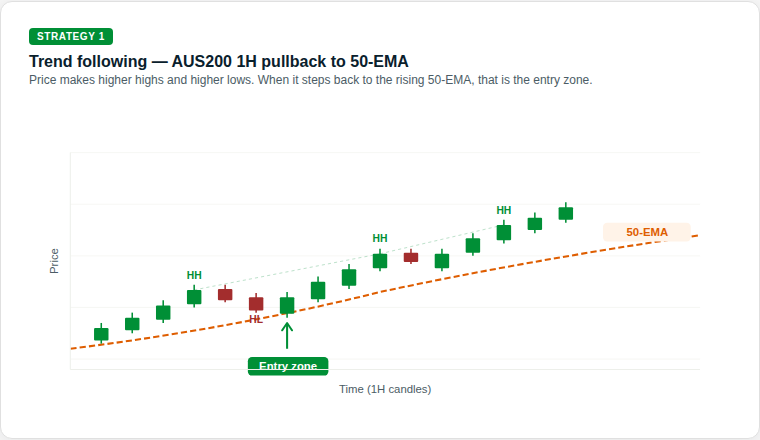

1. Mengikuti tren (permainan pendirian)

Trend follow bekerja pada gagasan bahwa pasar yang sudah bergerak dapat tetap bergerak sampai bertemu dengan hambatan struktural yang jelas. Beberapa pelaku pasar melihatnya sebagai pendekatan berbasis grafik karena berfokus pada arah yang berlaku daripada mencoba menyebut titik balik yang tepat.

Alasannya: Tujuannya adalah untuk mengidentifikasi bias arah yang jelas, seperti tertinggi yang lebih tinggi dan terendah yang lebih tinggi, dan mengikuti momentum itu daripada posisi melawannya.

Apa yang dicari pedagang: Rata-rata pergerakan eksponensial (EMA), seperti EMA 50 hari atau 200 hari, biasanya digunakan untuk menafsirkan kekuatan tren, meskipun indikator dapat menghasilkan sinyal palsu dan tidak dapat diandalkan dengan sendirinya.

Sumber: GO Markets | Contoh pendidikan saja.

Cara kerjanya: EMA 50-periode dapat bertindak sebagai level support dinamis yang naik seiring kenaikan harga. Dalam tren naik, beberapa pedagang mengawasi pasar untuk membuat level tertinggi baru yang lebih tinggi (HH), kemudian menarik kembali ke arah EMA sebelum bergerak lebih tinggi lagi. Setiap level rendah yang lebih tinggi (HL) mungkin menunjukkan pembeli masih memegang kendali.

Ketika harga menyentuh atau mendekati EMA 50-periode selama pullback itu, beberapa pedagang memperlakukan area itu sebagai zona keputusan potensial daripada mengasumsikan tren akan berlanjut secara otomatis.

Apa yang harus ditonton: Urutan HH dan HL adalah bagian dari bukti struktural suatu tren. Jika urutan itu rusak, misalnya jika harga turun di bawah HL sebelumnya, tren mungkin melemah dan pengaturan mungkin tidak lagi bertahan.

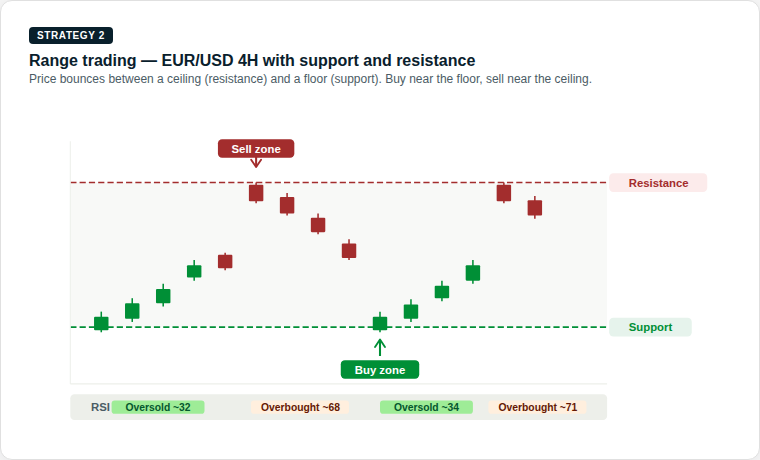

2. Range trading (permainan ping-pong)

Pasar dapat menghabiskan waktu lama bergerak ke samping. Itu menciptakan rentang, di mana pembeli dan penjual berada dalam keseimbangan sementara. Perdagangan rentang dibangun di sekitar perilaku ini, dengan fokus pada pergerakan di dekat bagian bawah dan atas kisaran yang ditetapkan.

Alasannya: Harga bergerak antara lantai, yang dikenal sebagai support, dan plafon, yang dikenal sebagai resistensi. Bergerak di dekat batas-batas tersebut dapat membantu menentukan lebar rentang.

Apa yang dicari pedagang: Beberapa pedagang menggunakan osilator seperti Relative Strength Index (RSI) untuk membantu menilai apakah aset terlihat overbuy atau oversold di dekat setiap batas.

Sumber: GO Markets | Contoh pendidikan saja.

Cara kerjanya: Level support adalah zona harga di mana minat beli secara historis cukup kuat untuk menghentikan pasar turun lebih jauh. Level resistensi adalah di mana tekanan jual secara historis mencegah kenaikan lebih lanjut.

Ketika harga mendekati support, beberapa pedagang mencari tanda-tanda potensi rebound. Ketika mendekati resistensi, mereka mencari tanda-tanda bahwa momentum mungkin memudar. Pembacaan RSI di bawah 35 dapat menunjukkan pasar oversold di dekat support, sementara pembacaan di atas 65 dapat menunjukkan bahwa pasar berada di atas pembelian di dekat resistensi.

Apa yang harus ditonton: Risiko utama dalam range trading adalah breakout, ketika harga mendorong secara tegas melalui kedua level dengan momentum yang kuat. Ini mungkin menandakan dimulainya tren baru dan menggunakan stop-loss tepat di luar kisaran pada setiap perdagangan dapat membantu mengelola risiko itu.

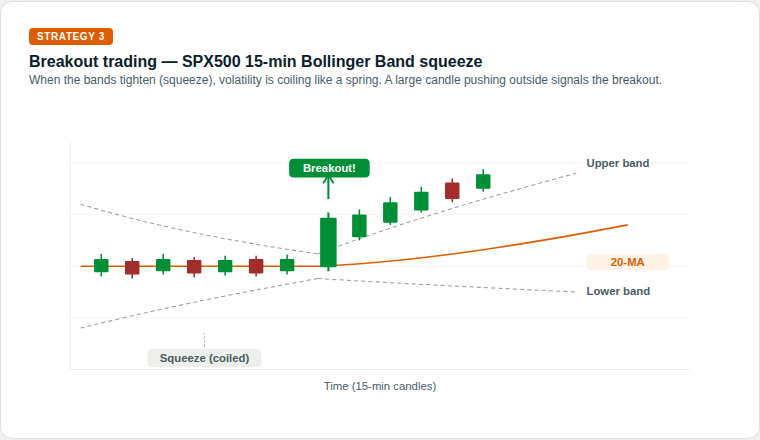

3. Breakouts (permainan pegas melingkar)

Akhirnya, setiap rentang berada di bawah tekanan. Terobosan terjadi ketika keseimbangan bergeser dan harga mendorong melalui support atau resistance. Pasar bergantian antara periode volatilitas rendah, di mana harga bergerak menyamping dalam kisaran yang ketat, dan ledakan volatilitas tinggi di mana harga dapat membuat pergerakan arah yang lebih besar.

Alasannya: Konsolidasi yang tenang terkadang dapat diikuti oleh ekspansi volatilitas yang lebih luas. Semakin ketat kompresi, semakin banyak energi yang dapat disimpan untuk langkah berikutnya.

Apa yang dicari pedagang: Bollinger Bands sering digunakan untuk menafsirkan perubahan volatilitas. Saat pita mengencang, tekanan terbentuk. Beberapa pelaku pasar melihat pergerakan di luar band sebagai tanda bahwa kondisi mungkin berubah.

Sumber: GO Markets | Contoh pendidikan saja.

Cara kerjanya: Bollinger Bands terdiri dari garis tengah, rata-rata pergerakan 20 periode, dan 2 pita luar yang berkembang atau berkontraksi berdasarkan volatilitas harga baru-baru ini. Ketika band-band menyempit dan saling berdekatan, tekanan, pasar menjadi sangat tenang.

Ini sering digambarkan sebagai pegas melingkar. Energi mungkin sedang berkembang, dan gerakan yang lebih tajam dapat mengikuti. Beberapa pedagang memperlakukan langkah pertama melalui pita luar sebagai petunjuk awal tentang arah, bukan sinyal definitif tersendiri.

Apa yang harus ditonton: Tidak setiap tekanan menyebabkan terobosan yang kuat. Terobosan palsu terjadi ketika harga bergerak sebentar di luar band, kemudian dengan cepat berbalik kembali ke dalam. Menunggu lilin menutup di luar band, alih-alih memasuki pertengahan lilin, dapat mengurangi risiko terjebak dalam gerakan yang salah.

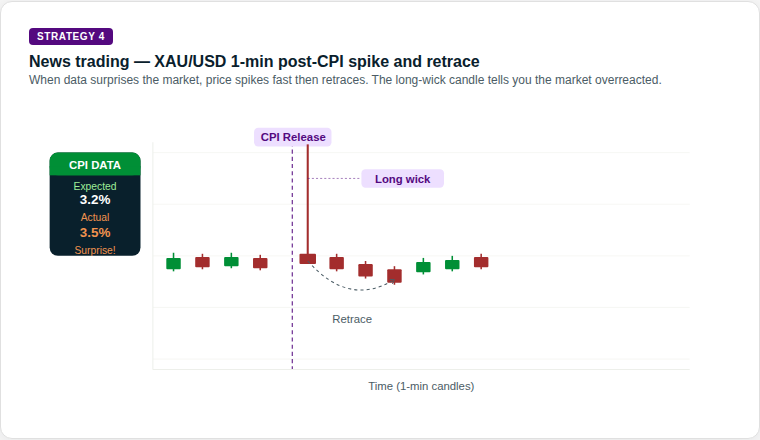

4. Perdagangan berita (permainan deviasi)

Ini adalah perdagangan yang digerakkan oleh peristiwa. Fokusnya adalah pada kesenjangan antara apa yang diharapkan pasar dan apa yang sebenarnya disampaikan oleh data atau judul. Rilis data ekonomi, seperti angka inflasi (IHK), laporan ketenagakerjaan dan keputusan bank sentral, dapat menyebabkan pergerakan tajam dan cepat di pasar keuangan.

Alasannya: Rilis berdampak tinggi, seperti data inflasi atau keputusan bank sentral, dapat memaksa repricing aset dengan cepat. Semakin besar kejutan relatif terhadap harapan, semakin besar pergerakannya.

Apa yang dicari pedagang: Pedagang sering menggunakan kalender ekonomi untuk melacak waktu. Beberapa fokus pada bagaimana pasar berperilaku setelah reaksi awal, daripada memperlakukan langkah pertama sebagai definitif.

Sumber: GO Markets | Contoh pendidikan saja.

Cara kerjanya: Sebelum berita, harga dapat bergerak dalam kisaran yang tenang dan ketat saat pedagang menunggu. Ketika data dirilis, jika pembacaan aktual berbeda secara signifikan dari ekspektasi konsensus, harga ulang dapat terjadi dengan cepat.

Emas, misalnya, dapat melonjak tajam pada pembacaan CPI yang berada di atas ekspektasi. Namun, lilin juga dapat mencetak sumbu atas yang sangat panjang, yang berarti harga mencapai lonjakan tertinggi tetapi kemudian ditolak dengan kuat. Penjual dapat masuk dengan cepat, dan harga dapat kembali. Pola spike-and-retrace ini adalah salah satu pengaturan yang lebih dikenal dalam perdagangan berita.

Apa yang harus ditonton: Arah dan ukuran lonjakan awal tidak selalu menceritakan kisah lengkapnya. Panjang sumbu dapat menawarkan petunjuk penting. Sumbu panjang mungkin menunjukkan gerakan awal ditolak, sementara sumbu yang lebih pendek setelah rilis data dapat menunjukkan gerakan arah yang lebih berkelanjutan.

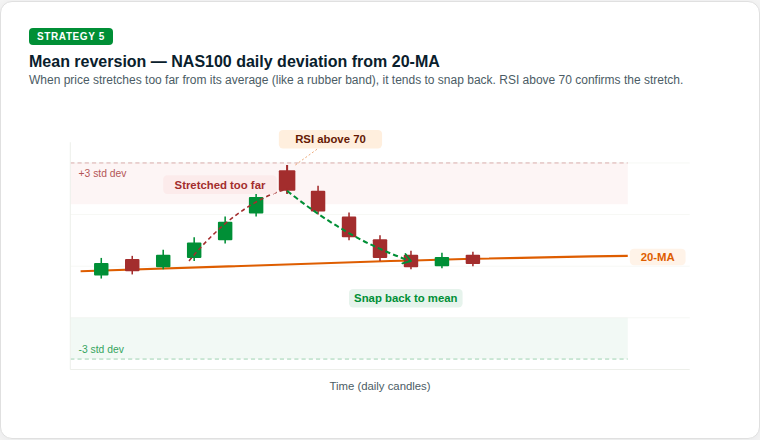

5. Pembalikan rata-rata (permainan karet gelang)

Harga terkadang bisa bergerak terlalu jauh, terlalu cepat. Pembalikan rata-rata dibangun di atas gagasan bahwa gerakan yang terlalu panjang dapat melayang kembali ke rata-rata historisnya, seperti karet gelang yang ditarik terlalu kencang, kemudian putus kembali.

Alasannya: Ini adalah pendekatan yang berlawanan. Ini mencari rentang optimisme atau pesimisme yang mungkin tidak berkelanjutan, dan posisi untuk kembali ke keseimbangan.

Apa yang dicari pedagang: Contoh umum adalah harga bergerak jauh dari rata-rata pergerakan 20 hari (MA) sementara RSI juga mencapai pembacaan ekstrem. Dalam pengaturan itu, pedagang memperhatikan pergerakan kembali ke rata-rata daripada kelanjutan menjauh darinya.

Sumber: GO Markets | Contoh pendidikan saja.

Cara kerjanya: MA 20-periode mewakili harga rata-rata pasar baru-baru ini. Ketika harga bergerak ke zona ekstrim, seperti lebih dari 3 standar deviasi di atas atau di bawah rata-rata itu, harga telah bergerak jauh dari tren baru-baru ini.

RSI di atas 70 dapat menunjukkan pasar membentang ke atas, sementara di bawah 30 dapat menunjukkan hal yang sama untuk sisi negatifnya. Beberapa pedagang reversi rata-rata menggunakan sinyal gabungan ini sebagai tanda bahwa kemunduran menuju MA 20-periode mungkin terjadi, daripada mengasumsikan pergerakan akan terus berlanjut.

Apa yang harus ditonton: Strategi reversi rata-rata dapat membawa risiko signifikan di pasar yang sedang tren. Pasar dapat tetap diperpanjang lebih lama dari yang diharapkan, dan posisi yang masuk melawan tren jangka pendek dapat menghasilkan penurunan besar. Ukuran posisi dan stop-loss yang jelas sangat penting.

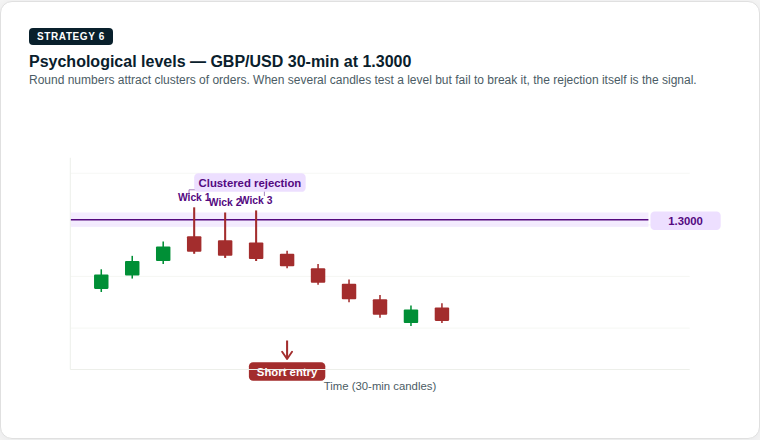

6. Tingkat psikologis (permainan tokoh besar)

Pasar didorong oleh orang-orang, dan orang cenderung fokus pada angka bulat. US $100, US $2.000 atau paritas 1.000 pada pasangan mata uang dapat bertindak sebagai magnet. Di pasar keuangan, tingkat harga tertentu dapat menarik jumlah aktivitas jual beli yang tidak proporsional, bukan karena analisis teknis saja, tetapi karena psikologi manusia.

Alasannya: Pesanan besar, stop-loss, dan level take-profit dapat mengelilingi angka-angka besar ini, yang dapat memperkuat dukungan atau resistensi. Perilaku yang memperkuat diri ini adalah salah satu alasan penolakan ini bisa menjadi bermakna bagi para pedagang.

Apa yang dicari pedagang: Pedagang sering memperhatikan bagaimana harga berperilaku saat mendekati angka bulat. Pasar mungkin ragu, menolak level atau menerobosnya dengan momentum. Beberapa penolakan sumbu pada tingkat yang sama dapat membawa lebih banyak bobot daripada satu penolakan.

Sumber: GO Markets | Contoh pendidikan saja.

Cara kerjanya: Ketika harga mendekati angka bulat dari bawah, beberapa pedagang memperhatikan sumbu atas yang panjang, garis vertikal tipis di atas badan lilin. Sumbu atas yang panjang berarti harga mencapai level itu, tetapi penjual melangkah masuk secara agresif dan mendorongnya kembali ke bawah sebelum lilin ditutup.

Satu penolakan sumbu mungkin penting. Tiga dalam satu cluster mungkin lebih signifikan. Beberapa pedagang menggunakan penolakan akumulasi ini sebagai bagian dari kasus untuk pengaturan pendek (jual) pada level itu.

Apa yang harus ditonton: Tingkat psikologis juga dapat bertindak sebagai magnet ke arah yang berlawanan. Jika harga menembus dengan keyakinan, level tersebut kemudian dapat bertindak sebagai dukungan. Penutupan yang menentukan di atas level, bukan hanya jeda sumbu, bisa menjadi tanda awal bahwa pengaturan penolakan tidak lagi bertahan.

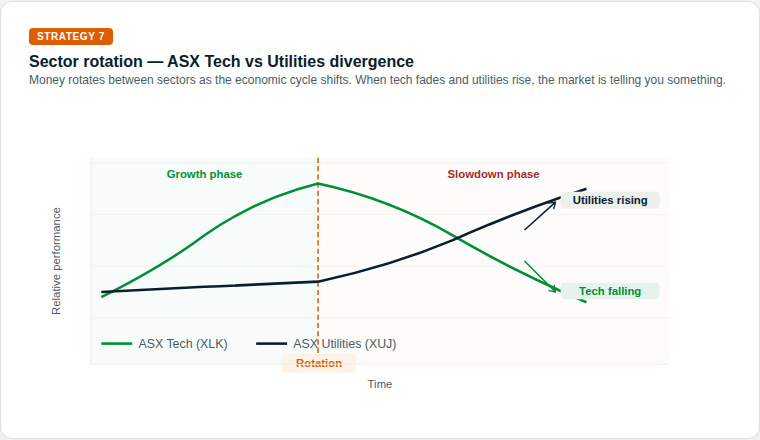

7. Rotasi sektor (permainan musim ekonomi)

Ini adalah strategi makro. Ketika latar belakang ekonomi berubah, modal dapat berpindah dari sektor yang tumbuh lebih tinggi ke sektor yang lebih defensif, dan kembali lagi. Tidak semua bagian pasar saham bergerak ke arah yang sama pada saat yang bersamaan.

Alasannya: Dalam perekonomian yang melambat, pengeluaran diskresioner dapat melemah sementara permintaan untuk layanan penting dapat tetap lebih stabil. Investor dapat merotasi modal antar sektor sesuai dengan itu.

Apa yang dicari pedagang: Dengan CFD, beberapa pedagang mengekspresikan pandangan ini melalui kekuatan relatif, mengambil eksposur ke sektor yang lebih kuat sambil mengurangi atau mengimbangi eksposur ke sektor yang lebih lemah.

Sumber: GO Markets | Contoh pendidikan saja.

Cara kerjanya: Selama fase pertumbuhan, ketika ekonomi berkembang, investor cenderung lebih memilih sektor yang berorientasi pertumbuhan seperti teknologi. Ketika lingkungan ekonomi bergeser, mungkin karena kenaikan suku bunga, memperlambat pendapatan atau meningkatnya risiko resesi, titik rotasi mungkin muncul.

Pada fase perlambatan, polanya bisa berbalik. Teknologi dapat melemah sementara utilitas dapat menguat, karena investor memindahkan modal ke sektor defensif yang menghasilkan pendapatan. Sinyal awal dapat mencakup kinerja relatif kurang di sektor pertumbuhan dikombinasikan dengan kekuatan yang tidak biasa dalam pertahanan.

Apa yang harus ditonton: Rotasi sektor biasanya bukan peristiwa semalam. Biasanya berlangsung selama berminggu-minggu hingga berbulan-bulan. Melacak rasio antara dua sektor, yang sering ditunjukkan dalam grafik kekuatan relatif, dapat membuat pergeseran ini terlihat sebelum menjadi jelas dalam hal harga absolut.

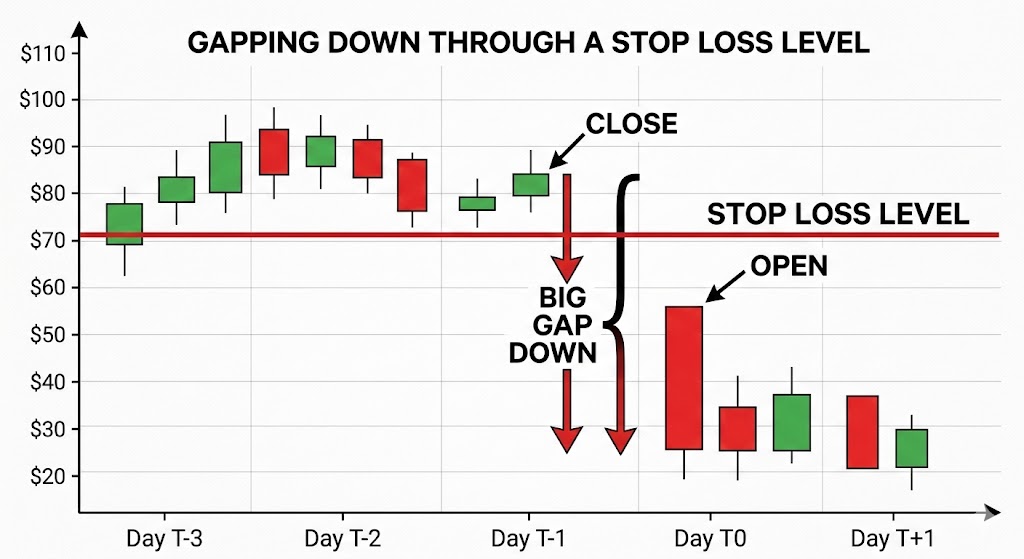

Mengapa manajemen risiko adalah mesin kelangsungan hidup

Langkah judul adalah satu hal. Implikasi pasar untuk akun Anda adalah hal lain. Jika Anda tidak mengelola mekaniknya, strateginya tidak masalah.

Karena CFD diperdagangkan dengan margin, pergerakan pasar kecil mungkin memiliki dampak besar pada akun. Jika leverage terlalu tinggi, bahkan goyangan kecil dapat memicu margin call atau penutupan posisi otomatis, tergantung pada persyaratan penyedia. Ini bukan risiko teoretis. Ini adalah alasan umum pedagang baru kehilangan lebih dari yang mereka harapkan pada perdagangan yang benar secara arah.

Pasar tidak selalu bergerak dalam garis lurus. Terkadang, kesenjangan harga dari satu level ke level lainnya, terutama setelah akhir pekan atau acara berita besar dan dalam kondisi tersebut, stop-loss mungkin tidak diisi dengan harga yang diminta tepat. Ini dikenal sebagai slippage. Ini adalah salah satu alasan mengapa posisi besar dapat membawa risiko tambahan ke dalam pengumuman besar.

Intinya

Kendaraan ini kuat, tetapi pedoman adalah apa yang membantu Anda tetap berada di jalan.

Perdagangan yang jelas seringkali sudah dihargai. Yang lebih penting adalah memahami kondisi pasar mana yang ada di depan Anda. Apakah itu sedang tren, rentang, pecah atau hanya bereaksi terhadap berita utama?

Pembaca yang menilai produk leverage sering fokus pada ukuran posisi, batas risiko, dan pengungkapan produk sebelum memutuskan apakah produk tersebut sesuai untuk mereka. Berita utama akan terus berubah. Matematika manajemen risiko tidak.

Siap untuk berdagang di luar mata uang utama? Buka akun · Masuk

Penafian: Artikel ini hanya informasi umum dan dimaksudkan untuk tujuan pendidikan. Ini menjelaskan konsep perdagangan umum dan perilaku pasar dan bukan merupakan saran produk keuangan, rekomendasi, atau sinyal perdagangan. Contoh apa pun hanya ilustratif dan tidak memperhitungkan tujuan, situasi keuangan, atau kebutuhan Anda. CFD adalah produk leverage yang kompleks yang membawa tingkat risiko tinggi. Sebelum bertindak, pertimbangkan PDS dan TMD dan apakah perdagangan CFD sesuai untuk Anda. Carilah saran independen jika diperlukan. Kinerja masa lalu bukanlah indikator yang dapat diandalkan untuk hasil masa depan.

Volatilitas memiliki cara untuk muncul tanpa diundang.

Suatu hari ASX melayang diam-diam... dan berikutnya, persyaratan margin naik, stop tidak terisi di tempat yang diharapkan, dan portofolio terbuka dengan celah semalam yang tidak nyaman.

Jika Anda telah mencari jawaban, Anda tidak sendirian. Beberapa pertanyaan yang paling banyak dicari tentang volatilitas di kalangan pedagang Australia berhubungan dengan margin call, slippage, gap semalam, leverage exchange trading funds (ETF), dan alat seperti rata-rata true range (ATR).

Inilah yang terjadi.

Mengapa ini penting sekarang

Pasar global menjadi lebih sensitif terhadap suku bunga, data inflasi, geopolitik, dan arus yang digerakkan oleh teknologi. Ketika likuiditas menipis dan ketidakpastian meningkat, perubahan harga melebar. Itu adalah volatilitas.

Dan volatilitas tidak hanya mempengaruhi arah harga, tetapi juga mengubah cara perdagangan dieksekusi, berapa banyak modal yang dibutuhkan, dan bagaimana risiko berperilaku di bawah permukaan.

Terjemahan: Volatilitas bukan hanya tentang pergerakan yang lebih besar, melainkan tentang pergerakan yang lebih cepat dan likuiditas yang lebih tipis - saat itulah mekanisme perdagangan paling penting.

Mengapa broker saya meningkatkan persyaratan margin?

Salah satu pertanyaan yang paling dicari tentang volatilitas adalah mengapa persyaratan margin meningkat tanpa peringatan.

Ketika pasar menjadi tidak stabil, broker dapat meningkatkan persyaratan margin pada kontrak untuk perbedaan (CFD) dan produk leverage lainnya. Perubahan harga yang lebih besar dapat meningkatkan risiko akun bergerak ke ekuitas negatif sehingga meningkatkan persyaratan margin mengurangi leverage yang tersedia dan dapat membantu mengelola eksposur selama kondisi ekstrem.

Apa artinya ini dalam praktiknya

-Margin call dapat terjadi bahkan jika harga tidak bergerak secara signifikan. Leverage yang efektif dapat turun dengan cepat. Posisi mungkin perlu dikurangi dalam waktu singkat.

Penyesuaian margin biasanya merupakan respons terhadap perubahan risiko pasar, bukan keputusan acak. Di pasar yang sangat fluktuatif, adalah bijaksana untuk mengasumsikan pengaturan margin dapat berubah dengan cepat, oleh karena itu banyak pedagang memilih untuk meninjau ukuran posisi dan buffer yang tersedia mengingat risiko itu.

Apa itu slippage dan mengapa stop saya tidak terisi dengan harga saya?

Topik lain yang sering dicari adalah selip.

Slippage dapat terjadi ketika stop order memicu dan dieksekusi pada harga yang tersedia berikutnya, hasilnya dapat bergantung pada jenis order, likuiditas pasar dan kesenjangan. Di pasar yang tenang, perbedaannya mungkin kecil sedangkan di pasar cepat, harga bisa berada di luar level stop.

Ilustrasi kesenjangan harga melalui level stop-loss | Pasar GO

Pengemudi umum termasuk

-Rilis ekonomi atau pendapatan utama. -Likuiditas tipis. -Tingkat pemberhentian yang penuh sesak. -Sesi semalam.

Order stop-loss umumnya memprioritaskan eksekusi daripada kepastian harga dan selama periode volatilitas tinggi, perbedaan ini menjadi penting. Menyesuaikan ukuran posisi dan menempatkan stop dengan mengacu pada pergerakan harga yang khas mungkin lebih efektif daripada sekadar mengencangkan stop dalam kondisi yang tidak stabil.

Bagaimana cara mengelola gap semalam di ASX?

Australia berdagang sementara Amerika Serikat tidur, dan sebaliknya. Sayangnya, perbedaan zona waktu ini adalah salah satu alasan mengapa risiko celah semalam sering dicari oleh pedagang Australia. Jika pasar AS turun tajam, ASX dapat dibuka lebih rendah keesokan paginya, tanpa peluang untuk keluar antara penutupan dan pembukaan.

Contoh pendekatan manajemen risiko yang dapat digunakan pedagang pasar meliputi

-Indeks lindung nilai menggunakan ASX 200 futures atau CFD*. -Lindung nilai sebagian selama peristiwa berisiko tinggi. -Mengurangi eksposur menjelang pengumuman makro utama.

Lindung nilai dapat mengimbangi bagian dari pergerakan, tetapi memperkenalkan risiko dasar karena saham individu mungkin tidak bergerak sejalan dengan indeks yang lebih luas.

Tidak ada perlindungan yang sempurna, hanya pertukaran antara biaya, kompleksitas, dan pengurangan risiko.

*CFD adalah instrumen yang kompleks dan memiliki risiko tinggi kehilangan uang karena leverage.

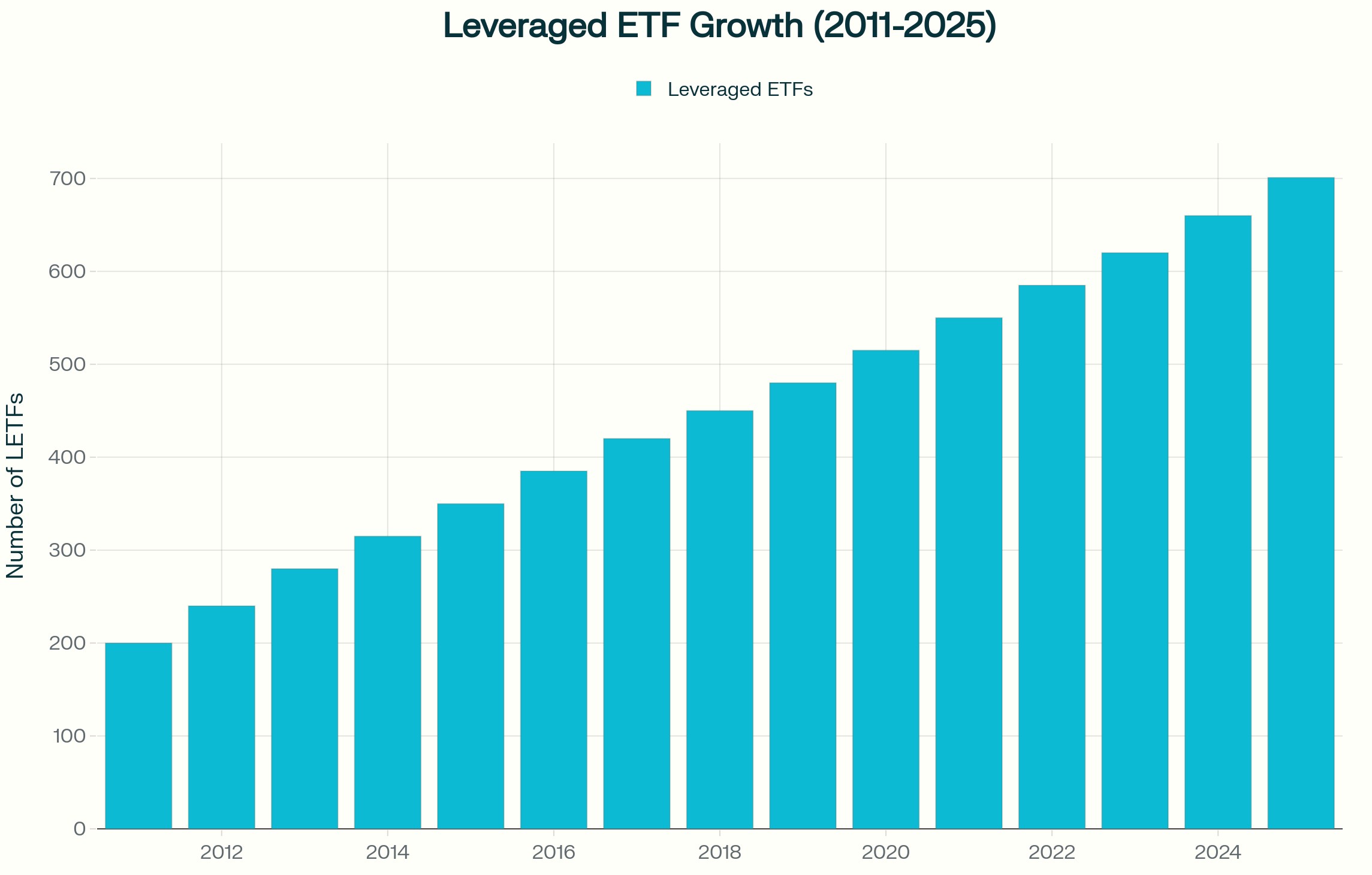

Apa risiko utama ETF leverage atau terbalik di pasar yang tidak stabil?

ETF leverage dan invers sering dicari selama periode volatilitas tinggi.

Meskipun produk-produk ini biasanya diatur ulang setiap hari, mereka bertujuan untuk memberikan kelipatan pengembalian harian indeks, bukan pengembalian jangka panjangnya. Di pasar yang bergejolak dan bergejolak, penggabungan harian dapat mengikis nilai bahkan jika indeks berakhir di dekat level awal.

Ini terjadi karena keuntungan dan kerugian bertambah secara asimetris. Penurunan 10 persen membutuhkan keuntungan lebih dari 10 persen untuk pulih. Ketika efek itu dikalikan setiap hari, hasil dapat menyimpang secara material dari indeks yang mendasarinya dari waktu ke waktu.

Instrumen tersebut dapat digunakan secara taktis oleh beberapa pelaku pasar. Mereka umumnya tidak dirancang sebagai alat lindung nilai jangka panjang dan memahami strukturnya sangat penting sebelum menggunakannya dalam strategi.

Bagaimana ATR dapat digunakan untuk menginformasikan penempatan berhenti?

Rata-rata true range (ATR) adalah indikator yang umum digunakan untuk mengukur volatilitas.

ATR memperkirakan berapa banyak aset biasanya bergerak selama periode tertentu, termasuk kesenjangan. Alih-alih menetapkan stop pada persentase sewenang-wenang, beberapa pedagang merujuk ATR dan menempatkan stop pada kelipatan, seperti dua atau tiga kali ATR, untuk mencerminkan kondisi yang berlaku.

Ketika volatilitas meningkat, ATR mengembang dan itu dapat menyiratkan stop yang lebih luas atau ukuran posisi yang lebih kecil jika risiko keseluruhan tetap konstan. Pergeseran adalah dari bertanya, “Seberapa jauh saya bersedia kalah?” untuk bertanya, “Apa langkah normal dalam kondisi saat ini?”

Pertimbangan praktis di pasar yang bergejolak

Selama periode volatilitas tinggi, pedagang dapat mempertimbangkan

Memungkinkan kemungkinan perubahan margin

Mengukur posisi secara konservatif jika volatilitas meningkat

Mengakui bahwa order stop-loss tidak menjamin harga keluar tertentu

Meninjau eksposur menjelang peristiwa ekonomi besar

Memahami mekanisme reset harian ETF leverage

Menggunakan ukuran volatilitas seperti ATR untuk menginformasikan penempatan berhenti

Mempertahankan buffer tunai yang memadai

Volatilitas tidak menghargai prediksi saja. Persiapan dan kesadaran risiko dapat membantu pedagang dalam memahami potensi risiko, tetapi hasilnya tetap tidak dapat diprediksi.

Pasar Australia menghadapi pertimbangan struktural spesifik yang dimapkan ke Pasar Asia dan AS. Risiko gap semalam dipengaruhi oleh jam perdagangan AS dan indeks sumber daya berat seperti ASX dapat merespons dengan cepat pergerakan harga komoditas dan data dari China. Eksposur mata uang, termasuk pergerakan AUD dan dolar AS (USD), dapat menambah lapisan variabilitas lainnya.

Volatilitas tidak seragam di seluruh wilayah. Ini berperilaku berbeda tergantung pada struktur pasar dan kedalaman likuiditas.

Pertanyaan yang sering diajukan tentang volatilitas

Apa yang menyebabkan lonjakan tiba-tiba dalam volatilitas pasar? Keputusan suku bunga, data inflasi, perkembangan geopolitik, kejutan pendapatan dan kendala likuiditas adalah pemicu umum.

Mengapa broker meningkatkan margin selama pasar yang bergejolak? Untuk mengurangi eksposur leverage dan mengelola risiko saat perubahan harga melebar.

Bisakah order stop-loss gagal selama volatilitas? Mereka dapat mengalami slippage jika pasar berada di luar level stop, yang berarti eksekusi dapat terjadi pada harga yang lebih buruk dari yang diharapkan. Di pasar cepat atau tidak likuid, perbedaan ini bisa signifikan.

Apakah ETF leverage cocok untuk lindung nilai jangka panjang? Mereka umumnya terstruktur untuk eksposur jangka pendek karena reset harian. Apakah mereka sesuai tergantung pada tujuan Anda, situasi keuangan, dan toleransi risiko.

Bagaimana volatilitas dapat diukur sebelum melakukan perdagangan? Alat seperti ATR, indikator volatilitas tersirat dan analisis rentang historis dapat membantu mengukur kondisi yang berlaku.

Peringatan risiko: Periode volatilitas tinggi dapat menyebabkan pergerakan harga yang cepat, perubahan margin dan eksekusi pada harga yang berbeda dari yang diharapkan. Alat manajemen risiko seperti stop-loss order dan indikator volatilitas dapat membantu dalam menilai kondisi pasar tetapi tidak dapat menghilangkan risiko kerugian, terutama ketika menggunakan produk leverage.

We are less than three weeks away from the ASX earning season and we are less than two weeks away from the earnings season in the US. So, we need to start prepping for trades and opportunities now. First and foremost, do not forget that confession season is well and truly upon us here in Australia.

Downgrades clearly have been coming from the discretionary sector; we've even seen companies hit the wall with the likes of Booktopia going into administration. There are some clear thematics that are growing in the Australian market. Energy, while the worst performing sector for the financial year 2024, may actually show you that earnings were slightly above expectation on higher than expected oil prices.

Materials led in the main by BHP, Rio and FMG Have once again benefited from higher than expected iron ore prices. It also benefited from a lower than expected AUD/USD where average FX prices were expected to be between $0.68 and $0.73 but instead have averaged between $0.63 and $0.67. What we're looking for is operational costs, overall margins and forward looking guidance, something that these firms have lacked in the last three financial updates.

Watch very closely for the excitement that will come from things like copper at the expense of the issues that are facing nickel lithium and other transition metals that have had really tough periods in FY24. Moving to the banks this is a sector people argue is fully valued. It's not hard to argue when through the financial year CBA made record all time highs several times and is still within a whisker of its record all time high.

Higher interest rates will indeed improve net interest margins. However, the unknown question and what we need to see at its August full year earnings is the impact higher rates are having on bad and doubtful debts, the possible increase in provisioning and more importantly the impact its having on new loans and refinancing. There is an argument to be made that banking is possibly fully priced and no matter what result is delivered won't necessarily create a leg further higher.

Finally, you can't go past consumer staples and discretionary. Retail sales numbers over the last 18 months have actually shown discretionary spending At or above 2022 levels although month on month figures have been erratic. The question that will come for discretionary spending is margins and how much sales revenue translates to the bottom line in earnings and profit.

Staples on the other hand have seen consistent movement on the revenue line but the question will be the margin and after the very targeted senate inquiry into supermarkets any sign profits are above trend may actually be met with concern as geopolitics raises its head. 33 times in 2024 the US 500 and the Tech 100 have made record highs – can it continue? Look into the US and the ending season that it is about to undertake. We have to look at several core thematics that are likely to be raised.

Artificial Intelligence (AI) The question you’ve got to ask is: is the time frame long or short? We raised this Mag 7 stocks etc Microsoft, Amazon, Alphabet, apple have clear potential. They are evolving their business models and see the integration of AI as the future of their individual businesses.

That will likely come up in their numbers but it will come with operational and initial upfront costs as the integration of AI begins. This is all long term may not fully capture short term opportunities which is still presenting very much in the semiconductor providers. NVIDIA and Advanced Micro Devices are taking full advantage and monetizing the compute cycle.

This clearly won't be forever because it will go from semiconductors to infrastructure to software and therefore the flows will move back towards the bigger end of town but overall the AI thematic still flows towards the semiconductors for now and that's likely to be shown in the earnings season that's coming. Data Centres That brings us to data centres because the potential for ensuring AI requires a heck of a lot of storage and a heck of a lot of processing. There are estimates the data centres will need to grow by 420% in Europe and 250% in the US by 2035 based on the rate of growth in AI right now.

Therefore, we need to watch providers like Dell Technologies and Intel which are big providers of data centres currently. We think the market hasn’t fully appreciated DC needs in the AI revolution. Cybersecurity The final key theme in the AI data centre technology space that we also think needs to be watched is cyber security.

It's been something along the lines of a 70% increase in ransomware attacks over the past 24 months. The regulatory requirements and the budgets required to deal with these increased threats is only just beginning. That brings players like Fortinet to the fore IT programmes and it's pensively to develop programs for enterprise makes it an interesting one going forward.

GLP-1 ‘Weight Loss’ Medicines Another theme of being a really strong driver of the S&P 500 is the rise of GLP-1 medicines. The weight loss craze that has come off the back of this Amazon has been incredible. Initially obviously developed for diabetes but having an additional effect of weight loss has created a product out of nowhere.

Eli Lilly and Co is a key player in this space with its GLP one class medicines already approved by the FDA. It's been launched in the US and its oral intake has posted adoption. It is not the only one in this space but shows very clearly the impact weight loss medicines are having on earnings.

The caveat we have though is side effects and long term impacts are still being found and could be said as a capping issue on price. Whatever way you look at it the US dating season however will be incredibly exciting and it is the reason The US markets continue to see huge capital inflows as they are much more exciting in this current environment than traditional value markets such as Australia.

Musim pendapatan AS April mendarat di pasar yang menginginkan lebih dari sekadar cerita bagus. JP Morgan telah menetapkan standar tinggi dengan hasil yang kuat, dan perhatian sekarang beralih ke ruang mesin S&P 500: infrastruktur AI. Tiga perusahaan berada di pusat cerita itu.

Mengapa jendela penghasilan ini penting untuk AI

Microsoft, Alphabet dan NVIDIA bukan hanya peserta dalam siklus AI, mereka membangun arsitektur fisik dan perangkat lunak yang bergantung pada perusahaan lain: chip, wilayah cloud, model, dan alat. Jika pengeluaran ini akan memberikan pengembalian, tanda-tanda pertama mungkin mulai terlihat dalam hasil triwulanan mereka selama beberapa minggu ke depan.

Setiap perusahaan mewakili tes yang berbeda.

Microsoft: Apakah adopsi AI perusahaan diterjemahkan ke dalam ekspansi pendapatan dan margin

Alfabet: Apakah memiliki tumpukan penuh, dari chip ke cloud hingga distribusi, adalah keuntungan yang tahan lama atau hanya posisi yang mahal untuk dipertahankan

NVIDIA: Apakah siklus perangkat keras masih bertahan, dipercepat, atau mulai merata

Pada tahun 2026, pertanyaannya bukan lagi apakah investasi AI sedang terjadi, komitmen modal substansialnya dan sudah dinyatakan secara publik. Pertanyaannya adalah apakah pengeluaran itu menghasilkan pengembalian cukup cepat untuk membenarkan skala taruhan tersebut.

IMPORTANT: REPORTING SCHEDULES CAN CHANGE WITHOUT NOTICE. REPORTING DATES AND RELEASE TIMES ARE FROM COMPANY INVESTOR RELATIONS CALENDARS WHERE MARKED CONFIRMED; OTHERWISE THEY ARE GO MARKETS ESTIMATES. CONSENSUS EPS, REVENUE AND ANALYST-RANGE DATA ARE FROM THIRD-PARTY MARKET CONSENSUS SOURCES, AS OF 16 APRIL 2026 (AEST). COMPANY GUIDANCE, BACKLOG AND OPERATING METRICS ARE FROM THE LATEST COMPANY FILINGS OR RESULTS PRESENTATIONS UNLESS STATED OTHERWISE. FIGURES AND SCHEDULES MAY CHANGE WITHOUT NOTICE.

$MSFT| Q1 2026 REPORTING PERIOD

Microsoft Corporation

NASDAQ | Technology | 29 Apr 2026

Confirmed

Global Release Countdown (AMC)

00:00:00:00

Consensus EPS

US$4.04

Consensus Revenue

US$81.40bn

AU/ASIA30 Apr | 6:05 am

US/LATAM29 Apr | 4:05 pm

Market Intelligence: $MSFT

Analysis: Microsoft price drivers and scenarios

Azure Growth Target

37-38%

Constant currency projection

AI Contribution

+6-8 pts

Azure revenue from AI services

FY26 Capex

US$146bn

Total infrastructure spending

AVG

LOW US$3.86AVG US$4.04HIGH US$4.14

Microsoft is being tested on a specific question: can it turn heavy AI spending into margin expansion? A result above US$4.14 could ease concerns over "capex fatigue" and demonstrate whether Azure growth is re-accelerating alongside enterprise AI adoption.

Factors that could move the markets

Azure growth rate

Watch if constant-currency growth re-accelerates above 39%, suggesting AI workloads are filling new capacity rather than sitting idle.

Signal: Capacity Utilisation

Workplace agent adoption

The shift to autonomous agents is central. Clear enterprise uptake in Dynamics 365 supports the high-tier subscription thesis.

Signal: Software Monetisation

Maia 200 cost savings

If the in-house AI chip is lowering inference costs at production levels, gross margins may start to recover from recent compression.

Watch: Gross Margin Recovery

Regulatory backdrop

Ongoing scrutiny of cloud bundling practices remains a potential headwind; management commentary here is vital for the long-term view.

Watch: Bundling Compliance

Sentiment Analysis · Microsoft Corp.

Interactive scenario analysis: $MSFT

Select earnings outcome

AI Scaling Proof

Strong result, backed by real AI progress

EPS above US$4.14 and Azure re-acceleration above 39% could support the view that AI spending is starting to translate into commercial returns. Workplace Agents show measurable ROI and FY26 guidance is raised.

EPS Outcome

Above US$4.14

Cloud Signal

Accelerating

Guidance

Raised

Possible reaction

Strong rally

Sources & Data Methodology

Sources: Reporting dates and release times are from company investor relations calendars where marked Confirmed; otherwise they are GO Markets estimates. Consensus EPS, revenue and analyst-range data are sourced from Bloomberg and Earnings Whispers, as at 16 April 2026 (AEST). Company guidance, backlog and operating metrics are sourced from the latest company filings or results presentations. Any scenario analysis reflects GO Markets analysis. Figures and schedules may change without notice.

Expanded Coverage

Beyond the Chipmakers

As the "show me the money" year unfolds, discover how AI demand is impacting Tesla, NextEra, and Exxon.

Alphabet has transformed from a search business into a sprawling AI infrastructure play, and this result will test whether that transformation is delivering. The US$185 billion capex forecast for 2026 is extraordinary, close to double last year's spending. EPS is expected to decline slightly year on year, precisely because that infrastructure spending is consuming capital. The question is whether Google Cloud's growth is fast enough to show a credible path back to margin recovery, and whether Ironwood, the seventh-generation custom AI chip, is proving its cost-per-query advantage at scale.

$GOOGL| Q1 2026 REPORTING PERIOD

Alphabet Inc.

NASDAQ | Technology | 29 Apr 2026

Confirmed

Global Release Countdown (AMC)

00:00:00:00

Consensus EPS

US$2.64

Consensus Revenue

US$92.14bn

AU/ASIA30 Apr | 6:30 am

US/LATAM29 Apr | 4:30 pm

Market Intelligence: $GOOGL

Analysis: Alphabet price drivers and scenarios

Cloud growth

48% YoY

Compared with last quarter

Ironwood TPU

10x peak

Vs previous-generation chip

2026 Capex

US$185bn

Double last year's spending

AVG

LOW US$2.50AVG US$2.64HIGH US$2.80

Alphabet has shifted to being viewed as a broader AI infrastructure play. The question is whether Cloud growth can support a path back to margin recovery while the massive US$185bn infrastructure buildout absorbs capital.

Factors that could move the markets

Google Cloud momentum

Markets are watching if the 48% growth rate holds, specifically among customers using Ironwood TPUs for large-scale AI.

Signal: Enterprise AI Adoption

Search & AI overview

If compute-intensive AI summaries are monetising through ads, it supports core search economics in the AI era.

Focus: Search Economics

Capex & margin trajectory

With free cash flow under pressure from US$185bn capex, markets want to know when infrastructure investment will moderate.

Watch: Spending Ceiling

DOJ antitrust risk

Management commentary on the legal timeline for Chrome or Android divestiture appeals will influence how risk is priced.

Watch: Regulatory Remedies

Sentiment Analysis · Alphabet Inc.

Interactive scenario analysis: $GOOGL

Select earnings outcome

Efficiency Proof

Ironwood efficiency drives upside

EPS above US$2.80 and cloud growth above 45% suggest Ironwood is cutting costs and strengthening Google’s advantage faster than expected.

EPS outcome

Above US$2.80

Cloud Signal

Strong growth

Waymo

Accelerating

Reaction

Sentiment improves

Sources & Data Methodology

Sources: Reporting dates and release times are from company investor relations calendars where marked Confirmed; otherwise they are GO Markets estimates. Consensus EPS, revenue and analyst-range data are sourced from Bloomberg and Earnings Whispers, as at 16 April 2026 (AEST). Company guidance, backlog and operating metrics are sourced from the latest company filings or results presentations. Any scenario analysis reflects GO Markets analysis. Figures and schedules may change without notice.

NVIDIA: the hardware cycle read through

NVIDIA is no longer simply a chip company. It has become what analysts now describe as the central bank of compute, the entity whose product determines how much AI capacity the world can actually deploy.

The upcoming Q1 FY2027 result will test whether the new Vera Rubin R100 GPU architecture, which entered mass production ahead of schedule, is already contributing to revenue, and whether NVIDIA can sustain gross margins above 75% as inference, rather than training, becomes the dominant workload. Inference is more competitive and more price-sensitive than training, so margin resilience here matters.

$NVDA| Q1 2026 REPORTING PERIOD

NVIDIA Corporation

NASDAQ | Semiconductors | 20 May 2026

Confirmed

Global Release Countdown (AMC)

00:00:00:00

Consensus EPS

US$1.70

Consensus Revenue

US$78.42bn

AU/ASIA21 May | 6:30 am

US/LATAM20 May | 4:30 pm

Market Intelligence: $NVDA

Analysis: NVIDIA price drivers and scenarios

Revenue growth

73% YoY

Last quarter benchmark

Data centre share

91%+

Share of total revenue

Rubin R100

In production

Mass production began April 2026

AVG

LOW US$76bnAVG US$78bnHIGH US$81bn+

NVIDIA’s outlook depends on whether Rubin R100 can keep gross margins above 75% as inference becomes a bigger part of demand. Because inference is more price-sensitive than training, margins are the key test.

Factors that could move the markets

Rubin ramp-up

Watch whether Rubin production can scale smoothly without disrupting the Blackwell transition.

Signal: supply chain continuity

Inference margins

The key test is whether NVIDIA can keep gross margins above 75% as inference revenue grows.

Signal: pricing power holds up

Sovereign AI demand

Government-backed investment in Europe and the Middle East could broaden the base beyond hyperscalers.

Signal: market expansion

CUDA regulatory risk

Any US or European scrutiny of NVIDIA’s software advantage could move the stock regardless of the revenue result.

Signal: software moat under review

Sentiment Analysis · NVIDIA Corp.

Interactive scenario analysis: $NVDA

Select earnings outcome

Rubin ramp supports growth

Rubin ramp supports growth

Revenue above US$81 billion may suggest the Rubin ramp is tracking ahead of expectations. That could support the view that AI demand is broadening into sovereign AI and enterprise markets, helping extend visibility into 2027.

Revenue Outcome

Above US$81bn

Gross Margin

Above 75%

Workload

Inference strong

Reaction

Positive read-through

Sources & Data Methodology

Sources: Reporting dates and release times are from company investor relations calendars where marked Confirmed; otherwise they are GO Markets estimates. Consensus EPS, revenue and analyst-range data are sourced from Bloomberg and Earnings Whispers, as at 16 April 2026 (AEST). Company guidance, backlog and operating metrics are sourced from the latest company filings or results presentations. Any scenario analysis reflects GO Markets analysis. Figures and schedules may change without notice.

Why this reporting window matters for the broader market

Microsoft and Alphabet report on the same evening, 29 April, making the overnight session into 30 April one of the most information-dense points of the year for equity markets. For Australian traders, both results should be available by 6:30 am AEST on Thursday 30 April. That means price reactions may already be visible in US futures before the ASX opens.

NVIDIA reports later, in May, but it casts a long shadow over everything in between. The guidance the company gave for Q1 FY2027, US$78 billion in revenue, has set a benchmark the market has been tracking for months. If Microsoft and Alphabet's results suggest AI infrastructure demand has softened, that could reset expectations heading into NVIDIA's call. If both beat expectations and signal accelerating cloud growth, that could lift the floor for what NVIDIA may report.

That interconnection is what makes this cluster different from most earnings windows. The results do not just affect the individual companies. They also signal the health of an investment supercycle that has driven global equity market leadership for the past two years.

What could shift the picture

Three risks could change the narrative regardless of how the numbers print. Each one is worth understanding before the results land.

1

Capex fatigue

If both Microsoft and Alphabet report in line or below expectations while reaffirming enormous spending plans, the market may start pricing the risk that AI monetisation is slower than the spending implies. That is not a stock-specific concern. It would be a broader de-rating event, affecting the valuations of companies across the technology sector that are priced on the assumption that AI returns are coming and coming soon.

2

Regulatory escalation

The FTC investigation into Microsoft, the DOJ case against Alphabet, and emerging EU scrutiny of NVIDIA's CUDA software ecosystem are all active. A material legal development before the earnings calls, whether a new filing, a remedy announcement or a court ruling, could overshadow the financial results entirely. Regulatory risk in this sector is not theoretical. It is live and moving.

3

Competition from custom silicon

Microsoft's Maia 200 chip, Alphabet's Ironwood TPU, Amazon's Trainium and Meta's custom accelerators are all reducing how much the large cloud companies depend on NVIDIA hardware. If any of these companies signals a meaningful shift in its GPU procurement plans during the earnings call, that could create uncertainty around NVIDIA's forward order book, even if its own Q1 FY2027 results beat expectations.

The 2026 Reality Check

$MSFT

AI spend is shifting from cost to competitive advantage. The question is whether margins can follow.

$GOOGL

Vertical integration from chips to search to cloud may prove to be a moat, or an expensive position to defend.

$NVDA

This is the pulse of the AI hardware cycle, and a test of whether Rubin can keep the supercycle alive into 2027.

Bottom Line

Microsoft and Alphabet report on the same evening, 29 April. NVIDIA follows in late May. Together, they may offer the clearest read yet on whether the AI infrastructure buildout is generating returns fast enough to justify the extraordinary scale of capital being committed. The earnings per share (EPS) number is important. What management says about AI monetisation timelines, capex trajectories and competitive positioning may matter more.

Your next earnings setup starts here

Stay ahead of major beats, misses, and market surprises. Log in to your terminal, open a new account, or explore our dedicated earnings academy.

April’s US earnings season is landing in a market that wants more than a good story. As GO Markets highlighted in its recent defence earnings watchlist, this reporting period is arriving after a broader shift in what markets care about. It is no longer just about growth at any cost. Traders want to know what the numbers are saying beneath the surface.

Why these 3 names matter

In this part of the market, that brings Tesla, NextEra Energy and Exxon Mobil into focus. Each offers a different read on a key 2026 theme: autonomy, electricity demand and oil supply risk.

Tesla: is being judged on whether autonomy and energy can support the next stage of growth

NextEra: offers a window into rising power demand and the infrastructure needed to meet it

Exxon Mobil: sits at the centre of the oil and energy security story as supply risks stay in focus

Taken together, these three names help explain where attention may be shifting. The question is no longer just who has the strongest narrative, rather, who can show real demand, firmer margins and execution that holds up in a more complicated backdrop.

In 2026, AI power demand is pushing utilities, storage and grid capacity into sharper focus while at the same time, oil supply risk has brought energy security back into the market conversation.

IMPORTANT: REPORTING SCHEDULES CAN CHANGE WITHOUT NOTICE. REPORTING DATES AND RELEASE TIMES ARE FROM COMPANY INVESTOR RELATIONS CALENDARS WHERE MARKED CONFIRMED; OTHERWISE THEY ARE GO MARKETS ESTIMATES. CONSENSUS EPS, REVENUE AND ANALYST-RANGE DATA ARE FROM THIRD-PARTY MARKET CONSENSUS SOURCES, AS OF 14 APRIL 2026 (AEST). COMPANY GUIDANCE, BACKLOG AND OPERATING METRICS ARE FROM THE LATEST COMPANY FILINGS OR RESULTS PRESENTATIONS UNLESS STATED OTHERWISE. FIGURES AND SCHEDULES MAY CHANGE WITHOUT NOTICE.

$TSLA| Q1 2026 REPORTING PERIOD

Tesla Inc.

NASDAQ | Consumer Discretionary | 23 Apr 2026

Confirmed

Global Release Countdown (AMC)

00:00:00:00

Consensus EPS

US$0.41

Consensus Revenue

US$22.26bn

AU/ASIA24 Apr | 6:05 am

US/LATAM23 Apr | 4:05 pm

Market Intelligence: $TSLA

Analysis: Tesla price drivers and scenarios

Auto Gross Margin

17-19%

Target floor, excl. credits

Megapack Growth

+25% YoY

Projected energy deployment

Analyst range

US$0.32-0.48

EPS estimate range

AVG

LOW US$0.32AVG US$0.41HIGH US$0.48

The US$0.16 analyst range shows there is still a lot of uncertainty. The main question is how weaker vehicle deliveries compare with stronger, higher-margin energy storage contributions. A result above US$0.48 would suggest the autonomy and battery story is improving faster than the bear case expects.

Key factors that could move the result

Automotive gross margin

This is the most important number for Tesla’s core business. Markets want to see whether price cuts have started to settle, or whether margins are still under pressure.

Benchmark: 17% (excluding credits)

Energy storage (Megapacks)

This is the more durable growth story. Strong Megapack deployment and battery margins could help offset weaker vehicle deliveries

Focus: Storage growth versus pressure in the auto business

Full Self-Driving (FSD) & Robotaxi

This is the main narrative driver. Markets will watch for updates on FSD adoption and the robotaxi timeline to judge whether the move towards “physical AI” is becoming more credible.

Watch: Timing for next-generation autonomy technology

Regulatory credits

This is a quality check on the result. If EPS is boosted too much by credit sales, some traders may see the beat as less durable.

Watch: How much credit sales contribute to final EPS

Trade Execution: $TSLA

Earnings reaction framework: Q1 2026

Bull case

EPS above US$0.45, energy margins at 20%+ | FSD take rates rising

The result clears the top-tier analyst range. Commentary focuses on FSD scaling and Megapack production ramps rather than vehicle discounting. FY26 guidance is reaffirmed.

Possible reaction: stronger momentum, with short covering adding support

Base case

EPS between US$0.38 and US$0.43, auto margins stable | Near target

The result is close to expectations, but there is no major surprise from the energy business. The market stays focused on the robotaxi timeline. The initial move may be limited if the product mix looks unchanged.

Possible reaction: range-bound trading or a muted early response

Bear case

EPS below US$0.35, auto margins drop below 16% | Signs of FSD delays

The result misses even cautious expectations. Rising inventory suggests more discounting may be needed. The market starts to question whether the level of spending on AI and autonomy is too high.

Possible reaction: rotation out of the stock, especially if growth confidence weakens

Sentiment Analysis · Tesla Inc.

Interactive scenario analysis: $TSLA

Select earnings outcome

Growth momentum

Strong result, helped by energy and FSD

FSD and Energy do better than expected, which helps offset weaker car deliveries. Management gives the market more confidence that autonomy is getting closer to real revenue. Auto margins staying above 17% would also help.

EPS Outcome

Above US$0.45

Energy Signal

On track

Margins

At or above 17%

Likely Reaction

Strong rally

Sources & Data Methodology

Sources: Reporting dates and release times are from company investor relations calendars where marked Confirmed; otherwise they are GO Markets estimates. Consensus EPS, revenue and analyst-range data are sourced from Bloomberg and Earnings Whispers, as at 14 April 2026 (AEDT). Company guidance, backlog and operating metrics are sourced from the latest company filings, results presentations or investor relations materials unless stated otherwise. Any scenario analysis reflects GO Markets analysis. Figures and schedules may change without notice.

From autonomy to electricity

If Tesla is the market’s test of whether physical AI can become a business, NextEra is a test of whether the power buildout behind AI is starting to show up more clearly in utility economics.

That is what makes the shift from Tesla to NextEra interesting. One is about ambition and platform narrative. The other is about power, contracts, infrastructure and return on capital.

$NEE| Q1 2026 REPORTING PERIOD

NextEra Energy, Inc.

NYSE | Utilities | 24 Apr 2026

Confirmed

Global Release Countdown (BMO)

00:00:00:00

Consensus EPS

US$0.91

Consensus Revenue

US$7.17bn

AUSTRALIA (AEST)24 Apr | 9:35 pm

ASIA (UTC+8)24 Apr | 7:35 pm

Market Intelligence: $NEE

Analysis: NEE price drivers and scenarios

Backlog Conversion

~29.8 GW

Energy Resources total backlog

Growth Framework

8%+ Annual

Adjusted EPS growth through 2032

Analyst Range

US$0.88 - 1.06

Q1 estimate spread

AVG

LOW US$0.88AVG US$0.92HIGH US$1.06

Against the 2026 ‘year of proof’ theme, the key issue is whether upcoming results turn strategic announcements into clearer execution signals. NextEra is a test of whether the power buildout behind AI is starting to show up clearly in utility economics.

Trade Execution: $NEE

Earnings reaction framework: Q1 2026

Key signals to watch

Contract Quality

Watch for movement from customer interest (20+ GW) to signed large load agreements.

Signal: Large load monetization

Natural Gas Hub Strategy

Firmer milestones on the approved up to 10 GW natural gas buildout approved earlier this year.

Signal: Infrastructure execution

Funding Clarity

Monitoring the impacts of the US$2.3bn equity sale and any potential Japanese funding progress.

Signal: Financing risk management

Sentiment Analysis · NextEra Energy

Interactive scenario analysis: $NEE

Select earnings outcome

Execution Focus

"Utility Renaissance" validates via execution signals

EPS above US$1.06 shifts attention to execution. Management points to signed large load agreements and clearer milestones for natural gas buildout. Progress converting 29.8 GW backlog into construction-ready projects strengthens sentiment significantly.

EPS Outcome

Above US$1.06

Infrastructure Signal

Contracts Signed

Likely Reaction

Sentiment Strengthens

Sources & Data Methodology

Sources: Reporting dates and release times are from company investor relations calendars where marked Confirmed; otherwise they are GO Markets estimates. Consensus EPS, revenue and analyst-range data are sourced from Bloomberg and Earnings Whispers, as at 13 April 2026 (AEST). Company guidance, backlog and operating metrics are sourced from the latest company filings or results presentations. Any scenario analysis reflects GO Markets analysis. Figures and schedules may change without notice.

From power to oil

If NextEra reflects the electricity side of the real economy story, Exxon Mobil reflects the fuel side. That matters in a market where supply risk can still reset inflation expectations, shift sector leadership and change how traders think about defensiveness.

$XOM| Q1 2026 REPORTING PERIOD

Exxon Mobil Corporation

NYSE | Energy | 29 Apr 2026

Estimated

Global Release Countdown (BMO)

00:00:00:00

Consensus EPS

US$1.66

Consensus Revenue

US$82.47bn

AUSTRALIA (AEST)29 Apr | 8:30 pm

ASIA (UTC+8)29 Apr | 6:30 pm

Market Intelligence: $XOM

Analysis: XOM price drivers and scenarios

Liquids Pricing Effect

+$1.9B - $2.3B

Positive 1Q realized price support

Energy Products Timing

-$3.3B to -$4.1B

Unfavourable 1Q accounting drag

Analyst Range

US$1.60 - 1.85

Low to high Q1 estimate spread

AVG

LOW US$1.60AVG US$1.66HIGH US$1.85

Exxon is the clearest oil-linked test in the market. The key issue is whether stronger oil and gas pricing can outweigh volume disruptions (6% production hit) and massive negative timing effects from Energy Products.

Trade Execution: $XOM

Earnings reaction framework: Q1 2026

Key signals to watch

Price Support vs Volume

Did the $2.3B pricing tailwind absorb the 6% Middle East production disruption?

Signal: Realized price strength

Timing Reversibility

Management commentary on whether the $4.1B timing drag is strictly non-cash and accounting-related.

Signal: Quality of earnings beat

Guyana Execution

Operational updates on the core upstream portfolio to ensure the long-term growth story remains constructive.

Signal: Upstream resilience

Sentiment Analysis · Exxon Mobil

Interactive scenario analysis: $XOM

Select earnings outcome

Price Support

Pricing tailwind more than absorbed the disruption

EPS above US$1.85 suggests high realized pricing from liquids absorbed volume hits. Management indicates timing effects were less severe than feared, with constructive operational updates from Guyana and the broader upstream portfolio.

EPS Outcome

Above US$1.85

Timing Impact

Smaller than feared

Likely Reaction

Sentiment Strengthens

Sources & Data Methodology

Sources: Reporting dates from company investor relations (Estimated for April 29, BMO). Consensus EPS and analyst-range data from Bloomberg and Earnings Whispers as at 13 April 2026 (AEDT). Scenario analysis reflects evaluateions of internal energy considerations. Figures and schedules are subject to change without notice.

Bottom line

This late-April energy cluster is about more than three company reports. It is a live test of what the market wants to pay for in 2026.

Tesla can show whether autonomy and energy are becoming more than a promise. NextEra can show whether rising electricity demand is turning into practical utility growth. Exxon can show whether oil strength still translates into durable earnings power.

Taken together, they offer a useful read on the part of the market that looks more physical, more capital-intensive and, for many traders, more real.

Your next earnings setup starts here

Stay ahead of major beats, misses, and market surprises. Log in to your terminal, open a new account, or explore our dedicated earnings academy.

Pengumuman gencatan senjata 8 April dan diskusi paralel seputar gencatan senjata 45 hari belum menyelesaikan gangguan Selat Hormuz. Mereka, untuk saat ini, membatasi skenario terburuk, tetapi lalu lintas tanker tetap pada sebagian kecil dari tingkat normal dan permintaan Iran untuk biaya transit menandakan perubahan struktural, bukan yang sementara.

Apa yang dimulai sebagai konflik regional telah menjadi kejutan energi global, dan pertanyaan bagi pasar bukan lagi apakah Hormuz terganggu, tetapi seberapa permanen gangguan itu mengubah dasar harga untuk minyak.

Kuncinya yang menarik

Sekitar 20 juta barel per hari (bpd) minyak dan produk minyak bumi biasanya melewati Selat Hormuz antara Iran dan Oman, setara dengan sekitar seperlima dari konsumsi minyak global dan sekitar 30% dari perdagangan minyak laut global.

Ini adalah kejutan aliran, bukan masalah inventaris. Pasar minyak bergantung pada throughput berkelanjutan, bukan penyimpanan statis.

Jika gangguan berlanjut lebih dari beberapa minggu, Brent dapat bergeser dari lonjakan jangka pendek ke guncangan harga yang lebih luas, dengan risiko stagflasi.

Lalu lintas kapal tanker melalui selat turun dari sekitar 135 kapal per hari menjadi kurang dari 15 kapal pada puncak gangguan, pengurangan sekitar 85%, dengan lebih dari 150 kapal berlabuh, dialihkan, atau tertunda.

Gencatan senjata dua minggu diumumkan pada 8 April, dengan negosiasi gencatan senjata selama 45 hari sedang berlangsung. Iran secara terpisah telah mengisyaratkan permintaan biaya transit pada kapal-kapal yang menggunakan selat, yang, jika diformalkan, akan mewakili dasar geopolitik permanen pada biaya energi.

Pasar telah mulai berputar menjauh dari pertumbuhan dan eksposur teknologi terhadap nama energi dan pertahanan, mencerminkan pandangan bahwa kenaikan minyak menjadi biaya struktural daripada premi risiko sementara.

Institutional Grade Performance

Master the Markets with MetaTrader 5

Trade hundreds of instruments with superior speed and advanced technical analysis. Harness full EA functionality to execute your strategy.

Selat Hormuz menangani sekitar 20 juta barel per hari minyak dan produk minyak bumi, setara dengan sekitar 20% dari konsumsi minyak global dan sekitar 30% dari perdagangan minyak laut global. Dengan permintaan minyak global mendekati 104 juta barel per hari dan kapasitas cadangan terbatas, pasar sudah seimbang sebelum eskalasi terbaru.

Selat ini juga merupakan koridor penting untuk gas alam cair. Sekitar 290 juta meter kubik LNG transit setiap hari rata-rata pada tahun 2024, mewakili sekitar 20% dari perdagangan LNG global, dengan pasar Asia sebagai tujuan utama.

Badan Energi Internasional (IEA) telah menggambarkan Hormuz sebagai titik henti transit minyak yang paling penting di dunia, mencatat bahwa bahkan gangguan sebagian dapat memicu pergerakan harga yang terlalu besar. Minyak mentah Brent telah bergerak di atas US $100 per barel, mencerminkan keketatan fisik dan kenaikan premi risiko geopolitik.

Sumber: Administrasi Informasi Energi AS, tanggal 17 Juni 2025, menggunakan rata-rata harian 2024

Kapal tanker menganggur karena aliran lambat

Data pengiriman dan asuransi sekarang menunjukkan ketegangan secara real time. Lebih dari 85 kapal induk minyak mentah besar dilaporkan terdampar di Teluk Persia, sementara lebih dari 150 kapal telah berlabuh, dialihkan atau ditunda karena operator menilai kembali keselamatan dan asuransi. Itu akan meninggalkan sekitar 120 juta hingga 150 juta barel minyak mentah menganggur di laut.

Volume tersebut hanya mewakili enam hingga tujuh hari throughput Hormuz normal, atau sedikit lebih dari satu hari konsumsi minyak global.

Data pengiriman dan asuransi yang diperbarui sekarang mengkonfirmasi lebih dari 150 kapal telah berlabuh, dialihkan, atau tertunda, naik dari 85 yang awalnya dilaporkan. Cakupan konsumsi global 1,3 hari dari minyak mentah yang tidak digunakan tetap menjadi kendala yang mengikat: ini adalah kejutan aliran, bukan masalah penyimpanan, dan gencatan senjata belum diterjemahkan ke dalam throughput yang dipulihkan secara bermakna.

🌋 Trump, volatility and Hormuz.

As tariff shocks collide with a ten year extreme in oil positioning, the margin for error is zero. See the technical markers and safe haven pivots defining the current risk environment.

Pasar yang dibangun di atas aliran, bukan penyimpanan

Pasar minyak berfungsi pada pergerakan terus menerus. Kilang, pabrik petrokimia, dan rantai pasokan global dikalibrasi untuk pengiriman yang stabil di sepanjang jalur laut yang dapat diprediksi. Ketika aliran melalui titik henti yang membawa sekitar seperlima dari konsumsi minyak global dan sekitar 30% dari perdagangan minyak laut global terganggu, sistem dapat bergerak dari keseimbangan ke defisit dalam beberapa hari.

Kapasitas produksi cadangan, sebagian besar terkonsentrasi di OPEC, diperkirakan hanya 3 juta hingga 5 juta barel per hari. Itu jauh di bawah volume yang berisiko jika aliran Hormuz sangat terganggu.

GO Markets — Idle Tankers: Days of Cover

Oil market analysis

How long do idle tankers last?

135M idle barrels — days of cover against each demand benchmark

vs. Strait of Hormuz daily flow (20M bbl/day)

6.75 daysof Hormuz throughput covered

6.75 days

0

5

10

15

20

25

30 days

vs. Global oil consumption (104M bbl/day)

1.3 daysof world demand covered

1.3 days

0

5

10

15

20

25

30 days

vs. US Strategic Petroleum Reserve release (1M bbl/day)

135 daysof full SPR release pace covered

135 days — but SPR exists to replace this role

0

5

10

15

20

25

30 days

135M

idle barrels on tankers (midpoint of 120–150M range)

~33%

of daily Hormuz flow that is idle storage, not transit

<31 hrs

is all idle storage against global daily consumption

Indicative market trajectories based on disruption severity

Scenarios for the weeks ahead

1–2 WEEKS

Ceasefire catch-up

Markets face catch-up repricing. Brent could consolidate in the US$105–US$115 range as risk premia unwind. Brent may trade lower (US$95–US$110) if strategic stocks bridge the temporary shortfall.

2–4 WEEKS

Infrastructure blitz

Shifts to structural supply shock. Brent moving toward US$150–US$200 cannot be ruled out. This is the stagflation trigger where energy costs constrain central bank flexibility.

STRUCTURAL

Geopolitical floor

Iran's transit fee demand creates a permanent input cost. The pre-crisis price structure (US$60–US$70) may not return, embedded in insurance and freight rates.

Critical Threshold

US$120 remains the level at which energy inflation becomes a direct Federal Reserve policy problem.

Risiko inflasi dan limpahan makro

Dampak inflasi dari kejutan minyak biasanya datang dalam gelombang. Harga bahan bakar dan energi yang lebih tinggi dapat mengangkat inflasi utama dengan cepat karena biaya bensin, solar, dan listrik bergerak lebih tinggi.

Seiring waktu, biaya energi yang lebih tinggi dapat melewati pengiriman, makanan, manufaktur, dan layanan. Jika gangguan berlanjut, kombinasi peningkatan inflasi dan pertumbuhan yang lebih lambat dapat meningkatkan risiko lingkungan stagflasi dan membuat bank sentral menghadapi pertukaran yang sulit.

🛢️ Brent hits $100.

Exxon and SLB are leading the rotation out of tech. Get the price targets and technical support levels for the top 5 energy majors.

Tidak ada offset yang mudah, sistem dengan sedikit kelonggaran

Apa yang membuat episode saat ini sangat akut adalah kurangnya kelonggaran dalam sistem global.

Pasokan dan permintaan global mendekati 103 juta hingga 104 juta barel per hari meninggalkan sedikit bantalan cadangan ketika chokepoint penanganan hampir 20 juta barel per hari, atau sekitar seperlima dari konsumsi minyak global, terganggu. Diperkirakan kapasitas cadangan 3 juta hingga 5 juta barel per hari, sebagian besar di dalam OPEC, hanya akan mencakup sebagian kecil dari volume yang berisiko.

Rute alternatif, termasuk jaringan pipa yang melewati Hormuz dan mengalihkan rute pengiriman, hanya dapat mengimbangi sebagian arus yang hilang, dan biasanya dengan biaya yang lebih tinggi dan dengan waktu tunggu yang lebih lama.

Intinya

Sampai transit melalui Selat Hormuz dipulihkan dan dipandang aman secara kredibel, aliran minyak global kemungkinan akan tetap terganggu dan premi risiko meningkat. Bagi investor, pembuat kebijakan dan pembuat keputusan perusahaan, pertanyaan intinya adalah apakah minyak dapat bergerak ke tempat yang seharusnya, setiap hari, tanpa gangguan.

Market Opportunity

Don't just watch the squeeze. Trade the framework.

As positioning gaps hit decade extremes, access advanced charting tools and real time execution on the six key markets defining this cycle.

.jpeg)