市场资讯及洞察

4 月的美股财报季正降临在一个“不再满足于听故事”的市场。摩根大通 (JPMorgan) 已经以强劲的业绩拉高了门槛,现在的焦点正转向标普 500 指数的“动力室”:处于 AI 基础设施叙事核心的三家巨头。

为什么这一财报窗口对 AI 至关重要

微软、Alphabet 和英伟达不仅是 AI 周期的参与者,它们更是在构建其他企业所依赖的物理与软件架构:包括芯片、云区域、模型及工具。如果这些巨额支出注定要产生回报,那么第一波迹象理应在未来几周的季度业绩中开始显现。

每家公司都代表着一次不同的考验:

- 微软 (Microsoft): 检验企业级 AI 的采用是否正在转化为实际的营收增长和利润率扩张。

- Alphabet: 检验从芯片、云端到分发渠道的“全栈模式”,究竟是持久的竞争优势,还是仅仅一个代价高昂的防御头寸。

- 英伟达 (NVIDIA): 检验硬件周期是否依然保持强势、正在加速,还是已经开始进入平稳期。

在 2026 年,问题已不再是“AI 投资是否在发生”——资本承诺已经数额巨大且已完全公开。核心问题在于,这些支出产生回报的速度,是否快到足以证明这些豪赌的规模是合理的。

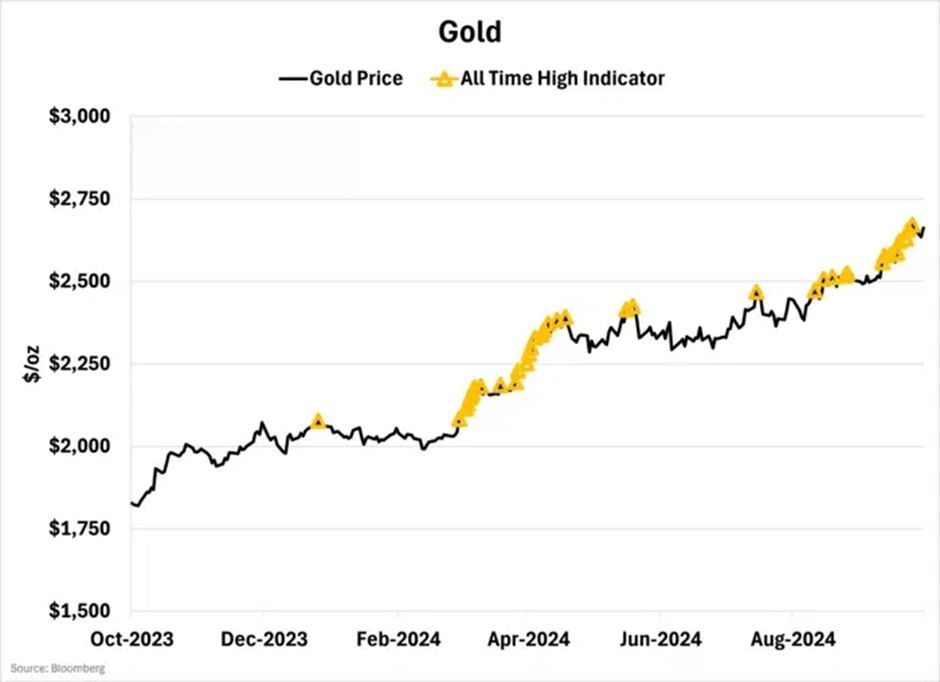

There's been plenty made this year about gold's incredible rise to new record levels. A point that gold bugs love to point out. As we sit here gold is trading at around US$2700oz having reached an all-time high that was just shy of US$2900oz.

Thus the question has to be asked: where is the limit? And where too from here for the inert metal? The movements over the last five years clearly suggest there is a structural change going on inside the very definition of what gold is. 14.7% in the last six months. 29.4% year to date. 34.2% in the last 12 months A staggering 82.3% in the last five years.

That is telling a story that is different to the original fundamentals we were taught at university and then as fundamental traders. Let's look at that theory: gold usually trades closely in line with interest rates, particularly US treasuries. As an asset that doesn't offer any yield it typically becomes less attractive to investors when interest rates are higher and usually more desirable when they fall.

That still technically holds true, However what has changed is how much central banks are interfering with that fundamental. Since 2022 when Russia invaded Ukraine one of the main reactions from the West was to freeze Russian central bank assets. Since that point the Russian central bank particularly has been buying gold as a form of asset store/reserve.

It has also allowed it to avoid the full force of financial sanctions placed on it. But they're not the only ones doing this; emerging market central banks have also stepped up their purchasing of gold since this sanction was put in place and are rapidly increasing their own central bank reserves. Then we look at developed markets central banks.

The likes of the US, France, Germany and Italy have gold holdings that make up to 70% of their reserves are net buyers in the current market. That suggests something else is afoot. Are they concerned about debt sustainability?

Considering the US has $35 trillion of borrowings which is approximately 124% of GDP, do central banks around the world see risk? Considering that many central banks have the bulk of their reserves in US treasuries coupled with the upcoming unconventional administration in the Oval Office this certainly puts gold’s safe haven status in another light. There are truly unknowns with the upcoming trump administration and gold is clear hedging play against potential geopolitical shocks, trade tensions, tariffs, a slowing global economy, deft defaults and even the Federal Reserve subordination risk So what is the outlook for Gold over the coming years and just how high could it go?

Consensus over the next four years is quite divided: by the end of 2024 the consensus is for gold to be at US$2650oz and then easing through 2025 to 2027 to $2475oz. However there are some that are calling for gold to reach the record reached in September this year before surging towards $2900oz the end of 2025 and holding at this level through most of 2026. And right now who could blame this prediction - Gold bugs believe the confidence in gold’s enduring appeal amid a volatile macroeconomic and geopolitical landscape is a bullish bet.

Expectations for sustained diversification and safe-haven flows do appear structural and with central banks and investors seeking to mitigate risks in an environment characterised by persistent uncertainty, geopolitical tensions, and economic volatility. And it's more than just the demand side that's leading the charge. The supply side of the equation further supports our bullish outlook.

Gold mine production is inherently slow to respond to rising prices due to long lead times for exploration, development, and production ramp-up. Furthermore, major producers avoid aggressive hedging strategies, as shareholders typically prefer full exposure to gold’s upside potential. The supportive fundamental backdrop reinforces that demand from both the official sector and consumers will remain robust, while supply-side constraints provide a natural tailwind for price appreciation.

What we as traders need to be aware of is many investors actually believe they've missed the rally and are wary of buying gold at all-time highs. There are some that believe gold is due pull back even a correction as they struggle to make sense of gold in the new world. The divergence away from yields coupled with unknowns out of China and the US has made them nervous to buy this rally.

But we would argue the pullback has probably already happened. If we look at the gold chart, since the US presidential election gold has moved through quite a reasonable downside shift. Dropping from its record all time high to a low $2530oz.

That decline has clearly been cauterised and the momentum now is clearly to the upside. We can see from the chart that spot prices are now testing the September-October consolidation period. Any clean break above these levels would see it going back to testing the head and shoulders pattern at the end of October-November.

This will be the keys to gold for the rest of 2024. But whatever happens in the short term the long-term trend suggests there is more for the gold bugs to delight in.

热门话题

11月20日盘后,英伟达(NVIDIA)发布了备受关注的2025财年第三季度财报。公司再次交出亮眼成绩单,营收和盈利均超市场预期。然而,尽管数据优异,这次市场反应却显得冷淡,收跌将近0.8%,但盘后股价一度下跌4%以上。那我们今天的文章就是来多角度看一下英伟达这次财报透露出的信息和这种现象发生的原因。

首先根据财报数据,英伟达第三季度营收达到351亿美元,同比增长17%,超出市场预期的347亿美元。净利润则同比激增至193.12亿美元,反映出其强大的盈利能力。数据中心业务成为增长主力,收入高达308亿美元,同比增长112%,这一表现再次巩固了英伟达在AI芯片市场的领导地位。游戏业务方面,营收达33亿美元,显示出稳定的市场需求。此外,英伟达的毛利率高达74.6%,刷新了历史记录,这得益于其高端AI芯片的定价策略和强劲需求。然而,公司也警告称,供应链瓶颈可能会在未来几个季度影响Hopper和Blackwell芯片的供应,这一消息的发出也导致市场对这次超出预期的财报并没有过于热情的反应。

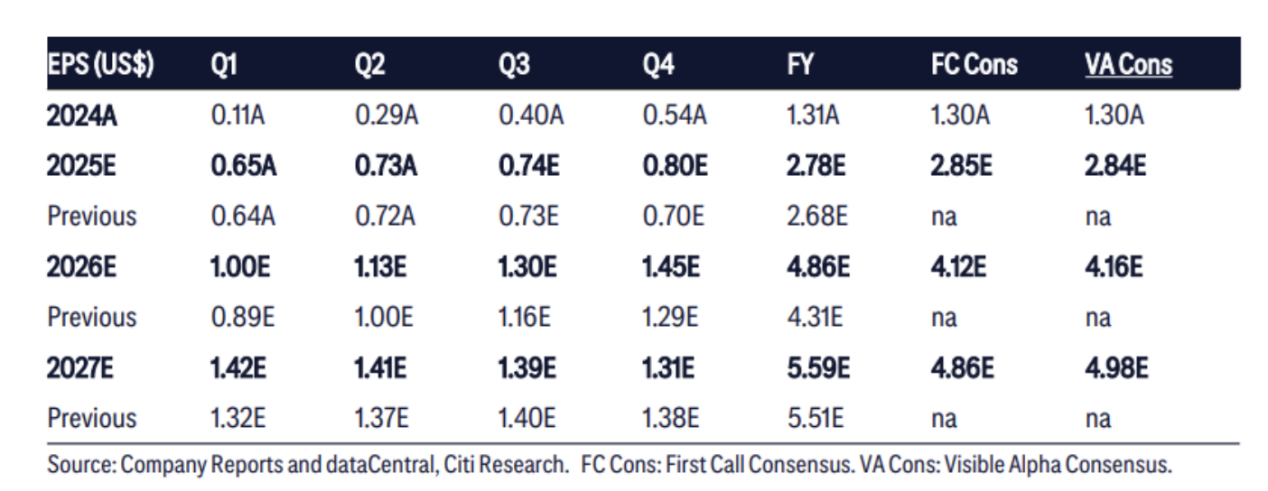

所以我们看到英伟达的股价在盘后交易中下跌4%以上,这也反映出投资者的复杂情绪。那么我们认为以下几个因素可能导致这一反应:高估值的压力英伟达当前市值接近1万亿美元,其股价已经包含了市场对未来增长的高度预期。尽管Q3财报超预期,但与上一季度的爆发式增长相比,增速明显放缓,投资者担忧这种趋势可能成为常态。供应链隐忧英伟达在电话会议中提到,Blackwell芯片的出货将在2025财年第四季度开始,但供应链限制可能持续至2026年。这一消息增加了投资者对公司未来营收增长的不确定性。短期业绩压力尽管数据中心业务表现强劲,但市场对未来几个季度的增长路径表现出谨慎态度。部分分析师认为,市场已经透支了对英伟达短期增长的预期,投资者期待看到更多新的增长点。尽管这次盘后的反应并不强烈,但是在人工智能浪潮下,英伟达仍然是最大的受益者之一。公司Hopper和Blackwell系列芯片的强劲需求,以及AI技术在更多行业的应用扩展,为其未来增长提供了坚实基础,比如我们所熟知的花旗银行就上调了英伟达2025财年、2026财年和2027财年的EPS预期,并把目标股价从150美元上调至170美元。

并且根据期权市场的数据我们会发现市场对英伟达财报的反应比对下月的非农、CPI和FOMC利率决议更为敏感,表明英伟达财报对市场(比如S&P500)的影响可能超过其他比较重大的经济事件了,这也表明英伟达的市场地位已经不容小觑。当然除此英伟达也在面临一些挑战:首先是面临的竞争压力,随着AMD、谷歌和亚马逊等巨头加速布局AI芯片市场,英伟达需要不断创新以维持其领先地位。此外,竞争对手在价格和性能上的追赶可能会对英伟达的市场份额和定价策略构成威胁。而放眼全球的宏观经济,全球经济增速放缓和高通胀可能压制企业对AI基础设施的投资,尤其是在利率高企的背景下。英伟达的增长依赖于数据中心和云计算领域的持续扩张,而宏观经济环境的不确定性可能对其增长产生拖累。以及我们前面提到过的供应链压力都可能在不同程度上影响英伟达未来的表现。

总体来说,这次英伟达的Q3财报再次证明了其在AI和芯片领域的强劲实力,但市场对其未来增长路径的期望已达极高水平,在高估值的背景下,短期的增速放缓和供应链隐忧成为压制股价的重要因素。未来,英伟达需要在技术创新、供应链优化和市场拓展方面继续发力才能保持行业领先地位。同时,投资者也是需要关注全球宏观经济环境、竞争格局变化以及AI技术的应用拓展,这些都将成为影响英伟达股价和增长的重要变量。当然了,我们还是认为无论是短期调整还是长期潜力,英伟达作为芯片界的领头老大,未来很长一段时间仍将是全球科技行业的风向标之一。免责声明:GO Markets 分析师或外部发言人提供的信息基于其独立分析或个人经验。所表达的观点或交易风格仅代表其个人;并不代表 GO Markets 的观点或立场。联系方式:墨尔本 03 8658 0603悉尼 02 9188 0418中国地区(中文) 400 120 8537中国地区(英文) +248 4 671 903作者:Yoyo Ma | GO Markets 墨尔本中文部

热门话题

在巴西二十国集团峰会期间举行的双边会晤中,澳洲总理阿尔巴尼斯和中国国家主席习近平讨论了两国关系的改善。为什么说近期是两国关系的转折点呢,核心是,特朗普重返白宫,承诺对所有进口到美国的商品征收高额关税,引发全球担忧。澳洲和中国在这个情况下,可能要加强双边贸易合作,将美国减少的市场份额,分配到其他国家和地区。如果我是澳洲总理,在特朗普上台的背景下,我会利用其贸易保护主义政策和全球经济格局的变化,推动澳大利亚实现更具战略性和多元化的国际贸易布局,同时在对中国态度和经济合作上采取灵活务实的策略。目前,总理阿尔巴尼斯宣布,和中国的“葡萄酒、木材、煤炭、大麦、海鲜等多个行业的贸易障碍已经消除,约 200 亿美元的贸易已经恢复。”

其实澳洲能做的,可以做的事情有很多,只要澳洲“公务员”稍微勤劳一些。当然,澳洲生活本来就是自由且缓慢的。但我们作为居民,仍然希望澳洲的经济能够更加繁荣。所以,借助特朗普全球战略收缩布局的背景,应该加强澳洲国际贸易领域的地位。首先扩大市场合作,减少对单一市场的依赖,包括对美国和中国部分领域的集中式出口或进口。最简单的就是加强与东南亚和南亚国家的合作,利用东盟的区域全面经济伙伴关系协定(RCEP),通过双边和多边贸易协议深化与东盟国家的合作。扩展与越南、泰国等制造业快速崛起国家的经贸关系,构建替代市场,降低未来输入性通胀的风险。借特朗普对欧洲盟友的疏远契机,与欧盟深化自由贸易协议(FTA)谈判,增加高附加值产品(如清洁能源技术和教育服务)的出口。在北美地区推动与加拿大和墨西哥的贸易合作,避免完全依赖美国市场。

其次,利用地缘优势,打造区域供应链枢纽。利用澳大利亚在印太地区的地理位置,主动融入全球供应链重组。澳洲到目前连个自己的汽车品牌都搞丢了,在制造业领域非常惨淡。但是中高端的供应链,可以加大国际人才和资本的吸引力度,鼓励国际企业在澳洲设立区域性物流、制造和数据中心,特别是在特朗普政策使供应链从中国转移的背景下。对中国方面,将中国作为战略贸易伙伴,但合作重点从资源出口转向高附加值领域。在清洁能源技术(如太阳能、电池存储技术)、农业科技和医疗设备方面寻求合作。鼓励中国对澳大利亚基建和高科技产业的投资,同时确保国家安全审查的透明性。大家想一想,如果澳洲几个城市,能够有高铁连起来,那么大家的出行,经济的发展,都会更进一步。当然,只是设想一下。在政策上,平衡中美关系,在对华政策上采取“不选边站”的态度。既通过与美国的盟友关系保护澳洲国家安全,又通过与中国的经济合作获取实惠。将中澳贸易争端诉诸世界贸易组织(WTO)等多边平台,避免双边摩擦升级。发展经济,藏富于民,增加人民收入和幸福指数,加强澳洲的综合实力,才是硬道理。在经济结构上,趁着美国回笼战略辐射范围的背景下,应该 推动国内经济转型,减少资源依赖:加大对高附加值产业(如人工智能、数字经济、农业科技)的支持,推动经济转型。加速清洁能源经济:发展澳洲丰富的太阳能、风能等清洁能源资源,将其出口至能源需求国(如日本、韩国)。建立出口多元化基金:为出口企业提供资金支持,帮助其开拓新兴市场。优化出口商服务:通过简化手续、税收优惠等措施,提升澳洲出口企业的国际竞争力。把美国放弃的合作,争取挖过来。填补美国退出的市场空白。

所以,总的来说,澳洲未来能够在经济领域,快速走出澳洲,用全球视野,做产业和经济结构转型和升级,引进国际人才和资本,输出本国特殊的经济产品,能够快速在国际社会上提升影响力,同时增加本土居民收入水平,降低单一合作伙伴或经济结构的潜在风险。金融领域,我认为中长期澳币还是要上涨,基于澳洲未来的经济机遇和大宗商品的推动,包括央行利率水平的稳定性,相比于特朗普,澳洲降息会滞后。同时,股票市场,目前情况下,BHP等矿业巨头股票,可能会在未来国际贸易中获益。大家可以关注中澳双边关系改善带来的贸易和投资机会。免责声明:GO Markets 分析师或外部发言人提供的信息基于其独立分析或个人经验。所表达的观点或交易风格仅代表其个人;并不代表 GO Markets 的观点或立场。联系方式:墨尔本 03 8658 0603悉尼 02 9188 0418中国地区(中文) 400 120 8537中国地区(英文) +248 4 671 903作者:Jacky Wang | GO Markets 亚洲投研部主管

热门话题

作为经常在股市或金融市场里的朋友们一定听说过美国高盛银行这个世界第一大投资银行的名字。作为美国华尔街的扛把子,高盛有着整个投资银行界几乎最高的平均收入,也一直是世界各国高校金融科目学子心中的第一圣地。想当年我在澳洲大学本科毕业也希望可以进入其中当一个初级分析师。现在知道了,绝大部分澳洲的投行只招收两种大学毕业生:背后资源丰富和毕业生,或本身硬实力顶尖的毕业生。这个其实放在哪里都一样,先不说。

相对于高盛在美国投行界的高收入,其在另一个领域也是相当的出名,就是之前多年来全球闻名的反向预测灯塔:也就是说,在过去多年的实践里,在多个重要的时间结点,高盛凭借其几乎100%的错误判断,成功的帮助了很多投资人亏得血本无归。但是同一时期,高盛公布的财报却又是节节攀升,这就奇怪了:你推荐给别人的产品,别人亏得毛都不剩,但是你自己却越赚越多?这背后原因无非两种:1.高盛自己买的都是不公开推荐的。2.高盛故意给别人推荐,自己再反向交易。当然,有鉴于美国华尔街相互之间都下黑手,所以如果高盛到不敢真的估计和客户反着来,这样一旦被发现,会被美国证监会罚的破产。所以大概率,高盛的投研部,和交易部根本就不沟通:投研部写的报告,交易部根本不用。好了,说了这么多背景介绍,现在来说重点:高盛最新的推荐:说2025年,黄金会到3000美元,高盛又说,2025年美元会继续保持强劲走势。按照高盛一贯的预测准确率,我们是不是可以反向猜测,就算不是两个全错,按理说至少有一个是错的。当然了,我们先来看看高盛给出的理由:就在上周日,11月17号,高盛分析师发布2025年展望报告,表示将继续看好黄金,并对贵金属领域最具信心。高盛将做多黄金列为其2025年大宗商品顶级交易(Top Trade)。根据高盛的预测,其判断在美联储降息的周期性和其他国家不断增加购买黄金的支持下,高盛维持对黄金3000美元的2025年年底目标价判断。

也就是说,从上周五收盘价格到3000的目标价格,还有至少17%左右的空间。除了看黄金到3000以外,高盛还给出了两个潜在更高的可能性:1. 如果特朗普上台以后发生贸易战,增加全球不确定因素。2. 美国财政因为不断增发国债导致可持续性危机。这两种情况都可能导致黄金价格超过3000美元大关。之后再来看看高盛对于美元走强的判断依据:高盛认为,2025年的外汇市场可能以美元的持续强势为主旋律。美国新政府政策组合的调整、美国经济的相对优势以及全球资本的流入,都为美元提供了支撑。因此高盛的投研团队改变之前对于美元看空的判断,反过来,预测美元的强势地位将比此前预期更持久。换句话,就是先啪啪打自己脸。之前的说了不算,重新预测。我估计是他们投研团队换了领导,所以之前的全部推翻,必须按照新领导说的写。当然,按照惯例,毕竟不是给自己亲爹意见,所以高盛还是很社会的留了一手:两头都要押注。他们说,尽管对美元保持乐观,但也指出了一些潜在风险因素:如全球其他经济增长超预期可能重新平衡全球资本流动,削弱美元的吸引力。其次,更大幅度的利率削减也可能对美元构成一定压力。总结一句话就是美元有可能涨,但是也不排除跌。是不是很鸡贼?

所以如果我们看高盛的预测,看完之后都是一个感觉:他到底要表达的是涨,还是跌?但是不论是涨,还是跌,三个月后,他们都可以找出一个更加充分的理由来推翻之前的看法,重新给出“精准而专业“的预测。市场里有个传言说,高盛的判断一般等你看到了,就意味着几乎他们所有的大客户已经建仓完毕,等外面的散户买入,开始接盘了。毕竟,如果你是投了几个亿的超级大客户,不可能和外面拿免费报告的小散在同一时间拿到报告。说了这么多,高盛还是那个高盛,他高概率的反向指标,依然无法动摇其美国第一投行的地位。但是对于我们在金融市场里危险冲浪的小散户而言,千万不要因为某一个机构的规模或头衔大而全信。一定要做到兼听则明,多听,多看,加上自己的思维,才能做到一个相对全面的理性分析。免责声明:GO Markets 分析师或外部发言人提供的信息基于其独立分析或个人经验。所表达的观点或交易风格仅代表其个人;并不代表 GO Markets 的观点或立场。联系方式:墨尔本 03 8658 0603悉尼 02 9188 0418中国地区(中文) 400 120 8537中国地区(英文) +248 4 671 903作者:Mike Huang | GO Markets 销售总监

热门话题

世界富翁马斯克最近喜事连连,不仅特斯拉股价暴涨140%,而且未来还可能成功跻身政坛,毕竟报恩的特朗普已经任命马斯克领导新一届政府下的“政府效率部”。虽然机构名称是“department”,但不是传统的内阁部门,更像是总统委员会(Presidential commission)。总统委员会是美国政府的外部建议机构,通常由外部专家组成,成立也比较简单,有总统行政令或备忘录即可,这意味着马斯克不用调整其在企业内的任职。马斯克虽然不进内阁,但是有总统的支持,他的权力不会小,市场上对于马斯克的政府工作宣传也很多了,总体来说,他的工作主要是削减联邦政府和支出。之前马斯克曾表示要削减2万亿美元支出,也就是砍掉约1/3的联邦政府支出,如果能成功实施,预计一定程度上可以抵消减税带来的赤字,不过可能会对就业造成影响。

马斯克不仅拥有特斯拉和SpaceX这两家科技巨头,还掌控着社交媒体平台X(前Twitter)。早在2021年,他的一个#bitcoin标签就让比特币在几小时内暴涨了19%;另一条“白银是新的GameStop”的推特甚至在短短几天内拉动银价上涨10%。而当他宣布要把特斯拉私有化时(尽管最终没兑现),TSLA股票当天大涨11%。但是到目前为止,马斯克对于黄金一直没有非常明确的态度。当马斯克全力为SpaceX铺平道路、甚至宣布了激进的火星计划时,他可能不得不关心黄金的价格,毕竟黄金不仅用于造飞船,火星上甚至可能有或可以合成黄金!首先我们来谈谈造飞船与黄金的关系。黄金是火箭和卫星的关键材料,可以帮助避免娇贵的电子设备生锈、腐蚀和损坏。黄金的高导电性可以实现信息在太空中的远距离传输,这对于卫星和空间站来说至关重要。由于黄金可以反射高达99.4% 的光粒子,因此它还可以用于降低太阳热量对航天器的热损耗,这也是为什么太空头盔的面罩上覆盖着一层薄薄的金子的原因,每个头盔的价格大约300 万美元,是地球上最昂贵的头盔之一了。哥伦比亚号航天飞机使用了约41公斤黄金,约合1,446盎司,而 SpaceX 与 NASA 签订了到 2030 年底的 50 亿美元合同,是仅有的与NASA签订商业补给服务(CRS-2)合同的三家公司之一。分析家预计全球航天工业到 2030 年将增长一倍,所以黄金需求将只升不降。

金矿作为一种稀缺品,需求越高,在地球就会越挖越深,就会越挖越少。根据世界黄金协会2024年最新统计,2023年地表黄金库存为212,582吨,大部分集中在1950年以后开采,而2024年三季度全球黄金需求总量(包括场外投资)同比增长5%,当然金价也连创新高,相信美联储降息前上车的朋友们收益不错。那么还有多少黄金可以挖呢?根据美国地质调查局研究,当前已探明储量约59,000吨,这意味着人类已经挖空了约3/4的金矿,结合金矿开采速度和各国金矿消耗速度粗略估计,剩余黄金平均只够挖20年了。

20年后,新增的黄金需求由哪里供给呢?SpaceX的火星计划或许给我们提供了无限可能。火星是一个巨大的红色星球,土壤环境和西澳矿山很接近,如果我们脑洞大开一下,“火星掘金”也不是完全不可能。

(火星地表图片)

(西澳矿山图片)科学家认为,外太空提供了火星合成黄金的环境条件:超新星爆炸、中子星合并和陨石撞击等宇宙事件会产生重元素,金就是其中之一。根据美国宇航局统计,火星每年遭受280到360 次陨石撞击,可能为金矿的产生提供了契机,而且火星上压力小,相比地球开采难度可能要低一些。

从SpaceX造价来说,马斯克显然希望金价越低越好,这样可以为SpaceX节省成本。但是我们认为,至少在实现火星采矿之前,黄金的需求仍是非常强劲的,至于20年之后会怎么样,就留给科技与科学吧!免责声明:GO Markets 分析师或外部发言人提供的信息基于其独立分析或个人经验。所表达的观点或交易风格仅代表其个人;并不代表 GO Markets 的观点或立场。联系方式:墨尔本 03 8658 0603悉尼 02 9188 0418中国地区(中文) 400 120 8537中国地区(英文) +248 4 671 903作者:Christine Li | GO Markets 墨尔本中文部

There has been plenty of conjecture about where oil is going to go in 2025 and we would suggest that the recent climb in Brent crude oil prices above $80 per barrel reflects an intensifying mix of geopolitical uncertainty. The main 3 uncertainties driving oil have been the impact of the U.S. presidential election, the escalation of the Middle East tensions and anticipation surrounding the OPEC+ meeting on December 1. These factors are clearly shaping short-term oil price dynamics, although some uncertainties have begun to ease, namely the election and the Middle East, but they still hold sway.

Thus let’s explore revised demand and supply projections as the industry anticipates a potential surplus in 2025 and the enactment of the Trump administrations Drill. Drill. Drill policy. 1.

Middle East Tensions Geopolitical tensions in the Middle East have posed a notable risk to the global oil supply particularly the conflicts involving Israel and Iran and the potential disruptions it would cause to OPEC’s 5 largest producers. However, so far, oil infrastructure in the region has largely remained intact, and oil flows are expected to continue without significant interruptions. While exchanges between regional powers remain a potential flashpoint, there is a general consensus that the two countries have stepped back from the worst.

The base case for this point is to assume stability in oil transportation routes and infrastructure. However, as we have seen during periods of unrest this year the consequences of a flare up for global oil prices can be considerable, underscoring the market's sensitivity to even minor shifts in Middle Eastern stability. 2. U.S.

Presidential Election – Drill Baby Drill The U.S. presidential election outcome has had a muted effect on oil prices – so far. This is likely due to President-elect Trump's policies regarding the energy being ‘speculative’. But there are several parts of his election platform that will directly and indirectly hit oil over the coming 4 years.

First as foremost – its platform was built on ‘turning the taps back on’ and ‘drill, drill, drill’. Under the current administration US shale gas and new oil exploration programs have come under higher levels of scrutiny and/or outright rejections. The new administration wants to reverse this and enhance the US’ output.

This is despite consensus showing these projects may return below cost-effective rates of return if oil prices remain low and the cost of production above competitors. Second, although President-Elect’s proposed tariff policies—ranging from 10-20 per cent on all imports, with higher rates on Chinese goods—could slow global trade, the net effect on the oil market is uncertain. Consensus estimates have the 10 per cent blanket tariff reducing U.S.

GDP growth by 1.4 per cent annually, potentially cutting oil demand by several hundred thousand barrels per day. If enacted, this bearish influence could counterbalance any potential bullish effects on prices. The third issue is geopolitics again – this time the possible reinstatement of the "maximum pressure" campaign on Iran that was enacted in the first Trump administration.

If the Trump administration imposes secondary sanctions on Iranian oil buyers, Iran’s exports could drop as they did during the 2018-2019 period, when sanctions sharply curtailed oil shipments. Such a development would likely tighten global supply and drive prices higher. These three issues illustrate possible impacts U.S. policy could have in 2025 and illustrate how contrasting economic and geopolitical factors could sway oil prices in unpredictable ways.

It again also explains why reactions in oil to Trump’s victory are still in a holding pattern. 3. What about OPEC? This brings us to the third part of the oil dynamic, OPEC and its upcoming Vienna convention on December 1.

The OPEC+ meeting presents another key variable, currently the consensus issue that member countries face - the risk of oversupply in 2025 and what to do about it. Despite Brent crude hovering above $70 per barrel, a price point that has normally seen production cut reactions, consensus has OPEC+ maintain its production targets for 2025, at least for the near term. We feel this is open for a significant market surprise as there is a growing minority view that OPEC+ could cut production by as much as 1.4 million barrels.

With Brent prices projected to stabilise around the low $70s, how effectively OPEC+ navigates this delicate balance between production and demand remains anyone’s guess and it's not out of the question that the bloc pulls a swift change that leads to price change shocks. December 1 is a key risk to markets. Where does this leave 2025?

According to world oil sites global supply and demand projections for 2025 suggest a surplus of approximately 1.3 million barrels a day, and that accounts for the recent adjustments to both demand and OPEC supply which basically offset each other. With this in mind and all variables remaining constant the base case for Brent is for pricing to sag through 2025 with forecasts ranging from as low as $58 a barrel to $69 a barrel However, as we well know the variables in the oil markets are vast and are currently more unknown than at any time in the past 4 years. For example: Non-OPEC supply growth underperformed in 2024, which is atypical; over the past 15 years, non-OPEC supply has generally exceeded expectations.

With Trump sworn in in late-January will the ‘Drill, Drill, Drill policy be enacted quickly and reverse this trend? This may prompt a supply war with OPEC, who may respond to market conditions by revising its output plans downward, which would tighten supply and support prices. In short its going to be complex So consensus has an oil market under pressure in 2025 with a projected surplus that could bring Brent prices into the mid-$60s range by the year’s end.

But that is clearly not a linear call and the global oil market faces an intricate array of challenges, and ongoing monitoring of these trends will be essential to refine forecasts and gauge the future direction of prices, something we will be watching closely.